Legal Design

The Idea

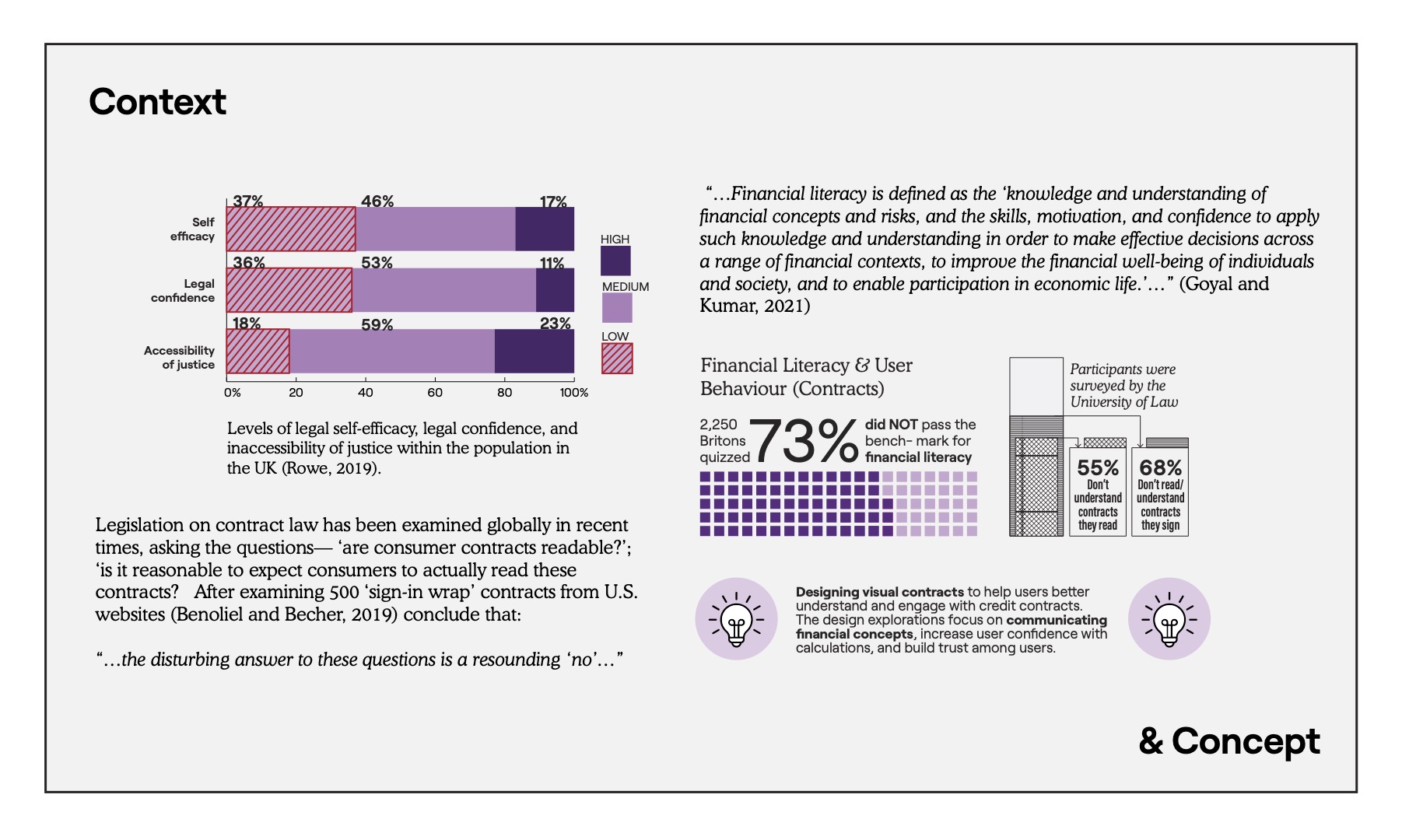

Designing visual contracts to help users better understand and engage with credit contracts. The design explorations focus on communicating financial concepts, increase user confidence with calculations, and build trust among users.

1.1 Concept

Designing layered visual contracts to help users better understand and engage with credit contracts. The design explorations focus on communicating financial concepts, increasing user confidence with calculations, and building trust towards financial intuitions/banks.This study will focus on literate adults in the UK as a target user group.

1.2 Background

In an increasingly digital world, with social media apps and countless platforms grabbing peoples’ attention, there is a decline in the attention span of the human population(Subramanian and Subramanian, 2018)While the problem of the decreasing attention span with respect to reading is a well-known one, and has been observed and recorded over decades, (Tanner, 2020) this project aims to address the challenges in consuming digital financial legal information specifically.

A. The Problem

A 2023 study conducted by the University of Law, UK, indicated that 68% of the questioned participants expressed that they don’t read/understand contracts that they sign for subscriptions and utilities. 55% of the people questioned claimed they did not understand what they were signing despite attempting to read their contracts. In the case of rolling contracts and subscriptions (checking updated ‘Terms and Conditions’), the numbers are more staggering with 82% of questioned participants claiming they don’t always check updated terms and conditions and 36% claiming they hardly/never check them (More than two thirds of people don’t read their contracts | ULaw, 2023).An experiment conducted in 2017, by Jonathan Obar of York University in Toronto and Anne Oeldorf-Hirsch of the University of Connecticut, revealed that 543 students agreed to the terms and conditions of a fictitious social networking company (NameDrop) which gave the company their future first born children. Agreeing to contracts or terms and conditions without fully understanding their implications can have life-altering consequences (Berreby, 2017).

B. Legal Literacy

According to a YouGov survey conducted in England and Wales a large percentage of the population have low-medium legal confidence, low-medium legal self-efficacy, and medium accessibility to justice (Rowe, 2019).

C. Financial Literacy

Another important consideration is financial literacy and capability. A systematic review conducted by (Goyal and Kumar, 2021) discusses these concepts—

“...Financial literacy is defined as the ‘knowledge and understanding of financial concepts and risks, and the skills, motivation, and confidence to apply such knowledge and understanding in order to make effective decisions across a range of financial contexts, to improve the financial well-being of individuals and society, and to enable participation in economic life.’...”

The review discusses the positive influence of financial literacy on financial behaviour such as saving, investing and debt management, while acknowledging other potential influencing factors such as culture and individual temperaments.

It also discusses the need for reform in the education of financial knowledge and notes a large gap in the field of debt literacy.

While the study reveals that developed countries have a higher financial literacy scores than that of under-developed ones, a study conducted in 2023 measuring the financial literacy (and creating a benchmark for the same) of 2,250 Britons through a quiz, reveals that 73% of the respondents fell below the benchmark with only 5% getting all 10questions in the quiz correct (What is the UK’s level of financial knowledge – and what impact is this having on our money?, 2024).

Research Question

How might interactive, visual information be simplified, grouped, and layered on a digital platform to increase comprehension of and engagement with financial legal information among literate adults in the UK?

2 Research Question

How might interactive, visual information be simplified, grouped, and layered on a digital platform to increase comprehension of and engagement with financial legal information among literate adults in the UK?

2.1 Sub questions & Areas of Exploration

- How might such an intervention reduce the cognitive load of users?

- How might such an intervention empower users to tackle financial calculations and increase confidence?

- How might such an intervention/the comprehension of such information affect the trust/confidence of users in financial institutions?

Literature Review—Key Insights

Legislation on contract law has been examined globally in recent times, asking the questions— “are consumer contracts readable?…the disturbing answer to these questions is a resounding ‘no’...”(Benoliel and Becher, 2019)

3 Literature Review

3.1 Legal Framework

The foundation of contract law in most countries, including the UK, is the duty of all parties to actually read a contract before agreeing to its terms—failing to do so will not serve as a viable reason to void a contract (I didn’t read the contract. Is it enforceable? | Pfeiffer Law,2020). Legislation on contract law has been examined globally in recent times, asking the questions—‘are consumer contracts readable?’; ‘is it reasonable to expect consumers to actually read these contracts? After examining 500 ‘sign-inwrap’ contracts from U.S.websites (Benoliel and Becher, 2019) conclude that:

“...the disturbing answer to these questions is a resounding ‘no’...”

Legislation in the UK seeks to address these problems through the CRA 2015, calling for intelligible and plain language contracts, along with guidelines from the Competition andMarkets Authority. However, such policies have gaps that do not define readability or the consumer for whom the contract must be readable. While certain states in the U.S. and other countries use reading scores such as Flesch-Kincaid as requirements for readable contracts, these are insufficient in assessing contracts due to their large scope for application and are not used in UK legislation. Further, contracts with technical terms, such as financial ones, face particular challenges with numerical and technical information. (Conklin, Hyde and Parente, 2019).

3.2 Digital Reading Habits

An investigation into on-screen versus print consumption of text showed that, particularly in the case of task focused reading, reading printed text led to greater comprehension and more focused reading (Delgado & Salmerón, 2021). Further, as studied by (Liu, 2021) on-screen reading resulted in a lack of focus due to distraction and multi-tasking behaviours.Such strategies and patterns must be considered when designing a digital solution for financial contracts.

While print reading forms a strong foundation for developing reading strategies, digital reading habits and challenges pose additional complexity and opportunities—users may feel overwhelmed when navigating various paths in non-linear reading which may also cause fragmented processing of information; multiple links and multimedia elements pose the risk of cognitive overload; and lack of in-depth reading due to scanning, skimming and skipping strategies are a studied phenomenon of digital reading in a hypermedia environment. Strategies employed for successful hypermedia reading relate to selective reading, strategic navigation, active engagement, and other cognitive strategies. These comprise of scanning and skimming through large pieces of information, planning a path to follow through the content, revisiting content, annotation and note-taking, interacting with elements, chunking information into smaller pieces, and monitoring one’s comprehension of the content (Titar-Improgo and Gatcho, 2020).

3.3 Math Anxiety

In designing a contract journey for a financial product, one must consider the fact of ‘math anxiety’. According to a study by (Ramirez, Shaw and Maloney, 2018) math anxiety maybe defined as:

“...feelings of fear, tension, and apprehension that many people experience when engaging with mathematics...”

The study notes 80% of community college and 25% of university students in the U.S.report having moderate to high levels of math anxiety, while (Hart and Ganley, 2019)suggest that women generally tend to face significantly higher levels of math anxiety.(Cheng et al., 2022) discuss math anxiety as an independent psychological construct that exhibits an increasing impact with age.

3.4 Existing Solutions

A recent empirical study by (Zan, Andersen and Toohey, 2023) on visual employment contracts used by two large Australian companies showed that visual contracts have the capability to reduce transaction costs of contracting, increase comprehension of and engagement with contracts (increasing the likelihood to read them), and foster positive attitudes towards the company. However, there is little work done to visualise financial legal contracts.

While simplified and visual contracts are being explored by various companies such as ‘Visual Contracts’, ‘Juro’, ‘Coffin Mews’, and ‘Majoto’, it is an emerging practice and requires more exploration. ‘Comic Contracts’ goes a step further and presents contracts in the form of comic strips for users with lower literacy levels (Botes, 2017). These solutions largely focus on text-based contracts. This project intends to focus on how to represent numerical data and financial concepts in credit contracts.

Outside of product driven solutions, prominent scholars such as Stefania Passera fromAalto University School of Science, Helena Happio from University of Vassa, and MargaretHagan from Stanford Law University have conducted research on legal design and visualcontracts.

(Haapio and Passera, 2016) argue that there needs to be a shift from ‘contract-drafting’ to ‘contract-design’ focusing not on the wording which predicts what courts would do, and rather on ‘comprehension’ by predicting what users would do, thereby adopting ‘preventative’ rather than ‘curative’ law practices. Their work, in this respect focuses on creating standards for visual contracts that curate to different audiences, making sure:

“...In a socio-technical system comprised of people, computers, and business/legalinformation, we need to ensure that people do not become the weak link...”

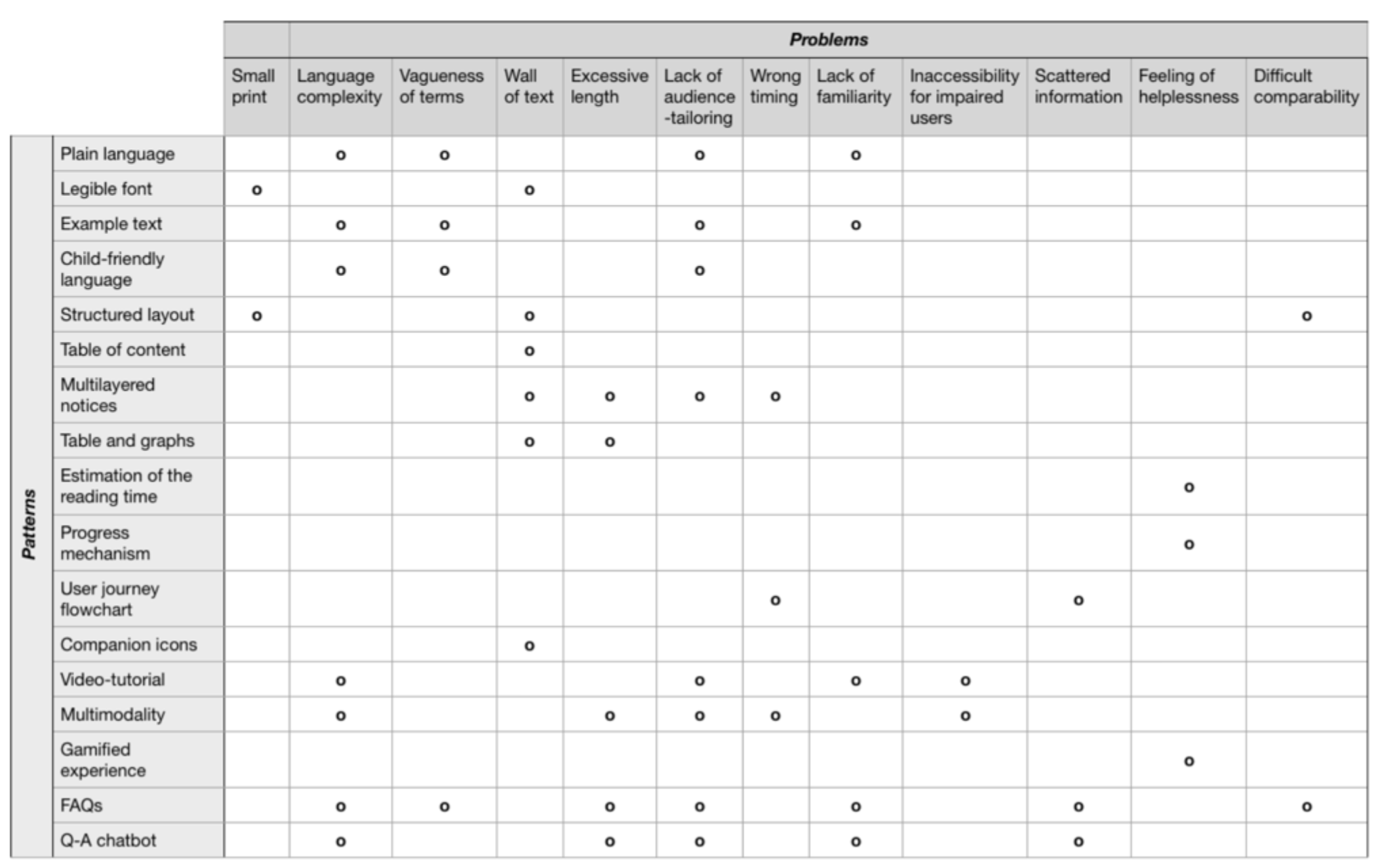

In ‘Legal Design Patterns’ (Rossi et al., 2019) visual contract design guidelines arediscussed to inform standardised and intelligible contracts. They address problems suchas small print, complex language, vague terms, intimidating walls of text, excessive length,and more. They do this through patterns that may solve these, such as plain language,legible font, structured layout, gamification and more (see image below).

3.5 State of the Art

In more recent work (Hagan, 2020) aims to develop research on ‘Legal Design’ practice, encouraging participatory networks, human-centred approaches that leverage technology (instead of being purely technology led) exploration, and long-term evaluation to make legal and justice instruments more accessible, equitable and usable. It suggests that solutions consider usability, enhancing the understanding of procedural justice, increasing engagement, helping achieve positive resolutions and reduce administrative burden. In (Legal Design Lab, 2024) we see this thinking in partnership with policy makers applied in projects that research the role of AI in access to justice, trying to understand what systems users want and how to regulate AI platforms; in eviction prevention endeavours; better forms and filing systems to encourage access to legal instruments; language support; and more. Such processes, while not in the scope of this project, must be considered and developed in the domain of private financial contracts in order to create large-scale positive impact on the financial health of a population.

There are also several Large Language Models (LLMs) that can perform legal reasoningprocesses, potentially providing legal aid to those who would otherwise be unable toreceive it. These models are emerging and do not yet have a place in the legal system—inthe legal domain any harms and mistakes would have to be carefully controlled andmitigated. Additionally, there are tools such as LegalBench that serve as benchmarks forLarge Language Models by assessing their legal reasoning capabilities across various legaldomains, tasks, and frameworks (Hoffman & Arbel, 2023).

Levels of legal self-efficacy, legal confidence, and inaccessibility of justice within the population in the UK (Rowe, 2019).

Primary Research

Participants were given a standard ‘Fixed Term Loan’ contract to read on screen while their eye gaze data was recorded, followed by a comprehension test, followed by a cognitive mapping workshop.

Primary Research

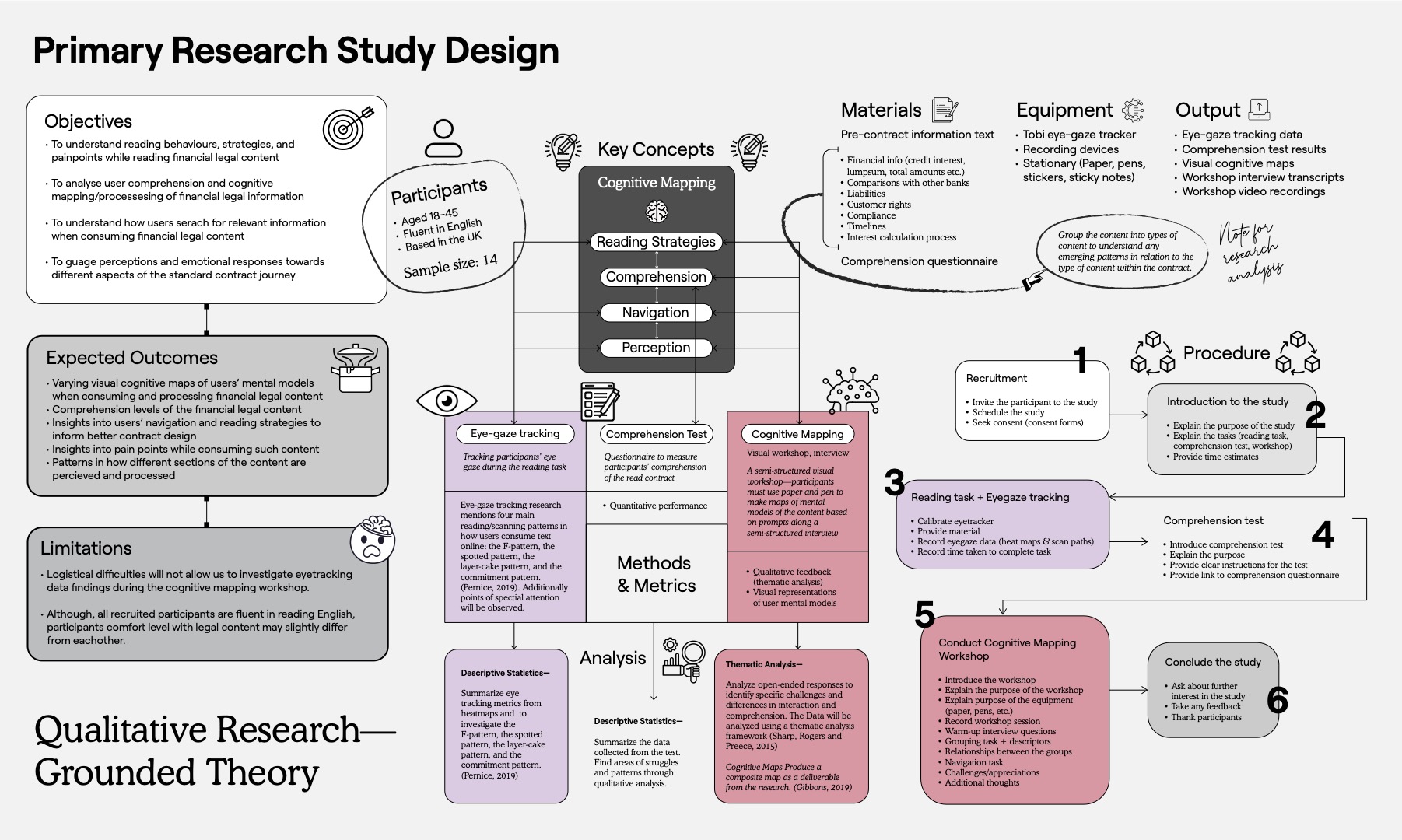

4.1 Methodology

Primary research was conducted using a qualitative approach through ‘Grounded Theory’to explore collected data in order to identify themes, patterns and common issues alongwith outliers (Tie, Birks and Francis, 2019).

4.2 Research Methods

An exploratory study was conducted to gain insights into user behaviour, comprehension and attitudes while consuming financial legal text.

A. Reading Task & Eye-gaze Tracking

Participants were given a sample ‘pre-contract’ of credit information to read on screen, while eye-gaze data was collected to assess reading strategies used during task-based reading. This task was timed.

B. Comprehension Test and Eye-gaze tracking

Participants were then given an on-screen comprehension test to assess the comprehension of the information consumed during the reading task. Here, they were allowed to refer to the materials from the reading task (pre-contract credit information)and use a calculator. This task was also timed.

C. Cognitive Mapping Workshop

Participants were then made to make visual maps (using a large sheet, markers, stickiesetc.) and answer questions about the concepts and experiences from the reading task and comprehension test. The aim was to gather data related to layering and grouping, insights into comprehension, emotional responses and perception, and insights into reading andinformation seeking strategies.

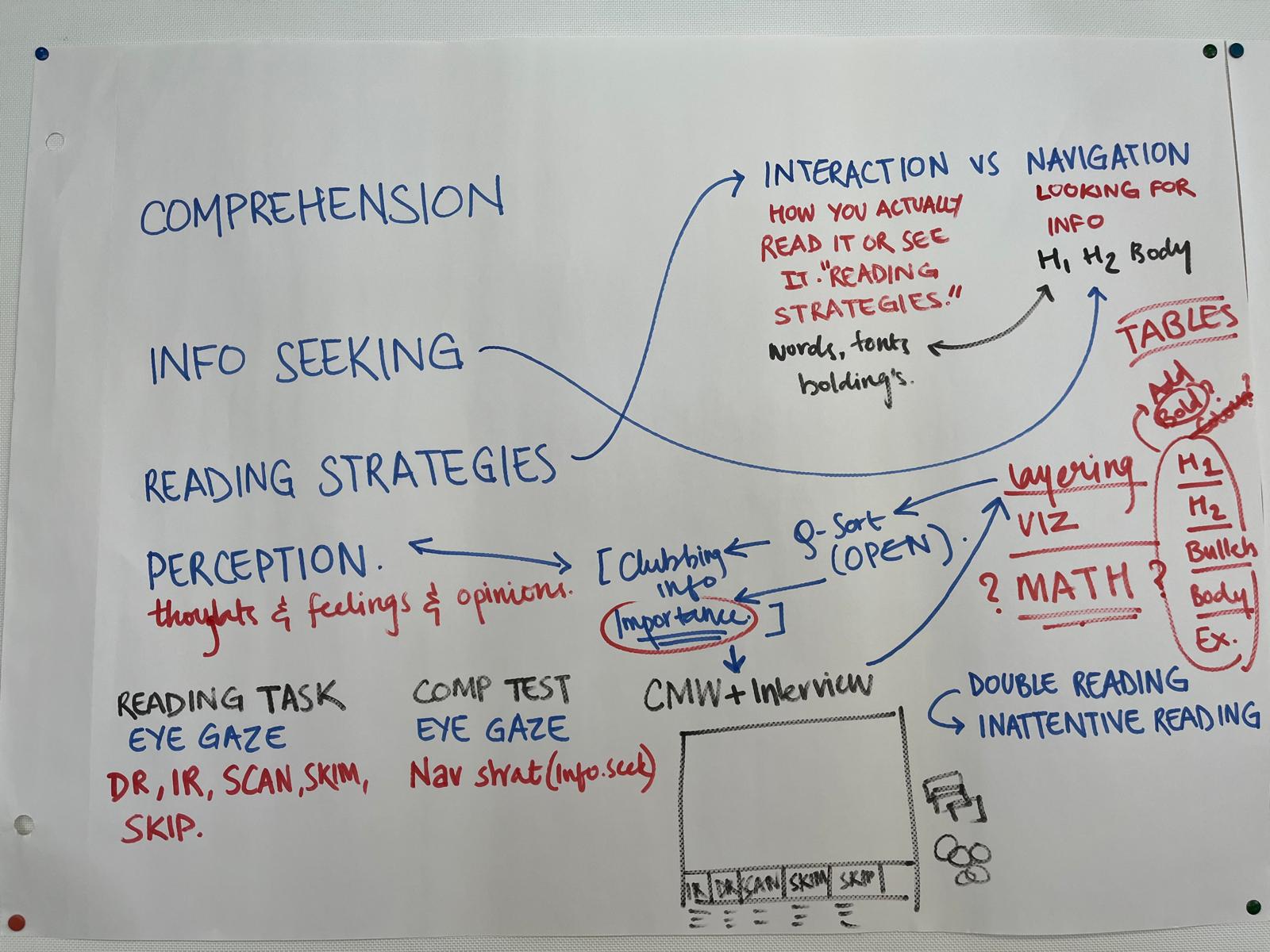

4.3 Key Concepts

The study was built around the following key concepts to gain valuable insights into user behaviours, attitudes and pain-points.

A. Comprehension

To understand how comprehendible the sample financial contract is. Particularly to understand user comprehension of interest rate and loan structure. Measured through the comprehension test and cognitive mapping workshop.

B. Information Seeking

To understand how users look for information using headings, bolded words, bullet points, tables and body text as anchor points. Measured via interview questions in the cognitive mapping workshop.

C. Reading Strategies

To understand how users consume a large piece of text. Looking for reading behaviours such as double reading, scanning, and skipping text through eye-gaze tracking. Measured additionally via interview questions in the cognitive mapping workshop.

D. Layering and Grouping

Understanding how users group and layer legal financial information. What is most important to users and what is unimportant but might be relevant. Measured through the Cognitive Mapping Workshop.

E Perception & Emotions

How users feel about numbers and calculations. What parts of the contract were frustrating and why? What strategies do they use to tackle anxiety about financial information. To be measured through the cognitive mapping workshop.

4.4 Experimental Design

A. Objectives

- To identify key challenges faced by users in comprehending financial credit contracts.

- To understand the reading and information-seeking strategies employed by users while consuming such contracts, especially when experiencing cognitive load.

- To identify mental models for grouping and layering sections of a financial contract among users, while assessing what they consider important/unimportant.

- To gain insights into the perception and emotional responses to the experience of reading such a contract and concepts within the same.

Note: a particular area of interest is how users experience, feel about and approach numerical/financial data and processes while dealing with such a contract, as it is essential in the successful comprehension of such a contract.

B. Participants

- Age 19–45

- Residing in the UK

- Fluent in English

C. Sample Size: 14

D. Location—

Goldsmiths University of London, UX Lab

E. Dates—

7th July 2024–11th July 2024

F. Roles

- Facilitator (moderator): Meghana Thakkar

- Note taker: Automatic transcriptions, video recordings

G. Materials (Appendix A)

Stimulus

A sample ‘Pre-contract Credit’ document outlining basic information about a credit/loan product and the lender, intended to help consumers decide whether the loan is right for them.

Comprehension Test

Assesses participants’ understanding of the contract content. Multiple choice questions using options tailored to the contract used for the study (Martínez, Mollica and Gibson, 2022)

Click to view comprehension test

Cognitive mapping workshop materials

Participants were given a large black sheet of paper along with printouts of separate clauses from the pre-contract document, markers, sticky-notes, and stickers to facilitate the workshop.

Semi-structured interview questionnaire for cognitive mapping workshop

A guideline of topics, tasks and questions to cover during the workshop. These tasks and questions were made to be flexible to gain rich data from participants.

Technology

Tobii pro Eye-gaze tracker, Microsoft Teams automated transcription, smartphone for video recording

H. Procedure

- The participants were recruited, made to sign consent forms, and were invited to the study. Here they were explained the purpose of the study and what it entails.

- They were made to sit in front of a screen where their eye-gaze was calibrated to the TobiiPro eye-gaze tracker after which the reading task was given on the same screen and timed.

- The reading task was immediately followed by the comprehension test. Users were allowed to refer to the document and use a calculator during the test which was also timed.

- The test was followed by an explanation of the cognitive mapping workshop. The cognitive mapping workshop was conducted where participants were asked to freely map out concepts from the contract and asked questions about their choices and experiences during the tasks in a semi-structured format. The workshop was video-recorded and later transcribed. The study was concluded here.

I. Metrics

Eye-gaze Tracking

Eye tracking is a sensor technology that can detect a person’s presence and follow what they are looking at in real-time. (www.tobii.com)

Eye-gaze tracking was conducted to identify reading and scanning patterns based on Nielsen Norman Group eye-gaze tracking research to find out how people read the contract and then use them to corroborate the data collected from cognitive mapping workshop. (Pernice, 2019).

Comprehension Test

Participants were given a comprehension test after completing the reading task. This was conducted to measure how much information they were able to understand. The overall score from the tests were recorded. (Quantitative performance) (Martínez, Mollica and Gibson, 2022) Subsequently, problematic areas of the contract were identified.

Cognitive Mapping Workshop

The participants were encouraged to put down the visual representation of their understanding of the contract. (Gibbons, 2019) A stereotypical cognitive map was produced as a deliverable from the research. (Gibbons, 2019) Themes from the transcripts recorded from the workshop were identified. (Sharp, Rogers and Preece, 2015)

Time taken for the reading task and comprehension test in order to identify and potential outliers for average time take to complete tasks.

J. Data Outputs

- Eye-gaze tracking data

- Comprehension test results

- Visual cognitive maps

- Workshop interview transcripts

- Workshop video recordings

K. Analysis Methods

Eye Gaze Tracking

Eye-gaze tracking research mentions four main reading/scanning patterns in how users consume text online: the F-pattern, the spotted pattern, the layer-cake pattern, and the commitment pattern. (Pernice, 2019).

The F-pattern

The F-pattern involves users reading across the top of a page and then moving down the left side(in languages written left to right), fixating on the beginning of each sentence creating an "F" shape.

The Spotted Pattern

The spotted pattern occurs when users focus on individual words or pictures that catch their attention due to being unique in style (font, bold etc) or match something required to complete the task at hand.

The Layer-Cake Pattern

The layer-cake pattern is characterised by users scanning the text, only fixating on headings, subheadings and/or pictures, often skipping the text in between.

The Commitment Pattern

When users read the text thoroughly from beginning to end, the commitment pattern is observed. This usually occurs when users trust the source of information or are deeply interested in the content. These findings make a strong case for optimising the content to align with these varied reading behaviours. (Pernice, 2019).

Comprehension Test

Descriptive Statistics: Summarise the data collected from the test to identify problem areas.

Cognitive Mapping Workshop

Open-ended responses from the interview were analysed to identify specific challenges in reading & information-seeking strategies, perception and comprehension. The data will be analysed using a thematic analysis framework (Sharp, Rogers and Preece, 2015). Cognitive Maps were used to produce a composite map with insights about layering and grouping as a deliverable from the research. (Gibbons, 2019).

L. Expected Outcomes

- Varying visual cognitive maps of users’ mental models when consuming and processing financial legal content

- Comprehension levels of the financial legal content

- Insights into users’ navigation and reading strategies to inform better contract design.

- Insights into pain points while consuming such content.

- Patterns in how different sections of the content are perceived and processed.

- Specific insights into user behaviours, attitudes, and challenges towards mathematical and financial concepts and procedures; particularly on support mechanisms to alleviate math anxiety and increase confidence for the same.

M. Limitations

- Logistical difficulties will not allow an investigation into eye-tracking data findings (from the reading task) during the cognitive mapping workshop.

- Although, all recruited participants are fluent in reading English, participants comfort level with legal content may slightly differ from each other.

N. Execution

A pilot study was conducted with 4 participants. The study was found to be too long, and the cognitive mapping workshop was too unstructured. The comprehension test was shortened and simplified to only multiple-choice questions and a semi-structured list of questions and tasks for the cognitive mapping workshop was formulated. Further, the sample contract was redesigned to avoid unnecessary reading problems such as poorly justified text and tables spanning across pages that are not relevant to the study.

The study was then conducted based on the changes from the pilot and the experimental design mentioned above.

Key Concepts

NAVIGATION

COMPREHENSION

READING STRATEGIES

PERCEPTION

MATHEMATICAL BEHAVIOURS

Key Insights/Findings

Variety of scanning techniques used to read the contracts

Anxiety about the late/missed payments section

Skipped through ‘unimportant’ information

Distrust in financial institutions

Most attention on numerical information

Many information gaps were identified

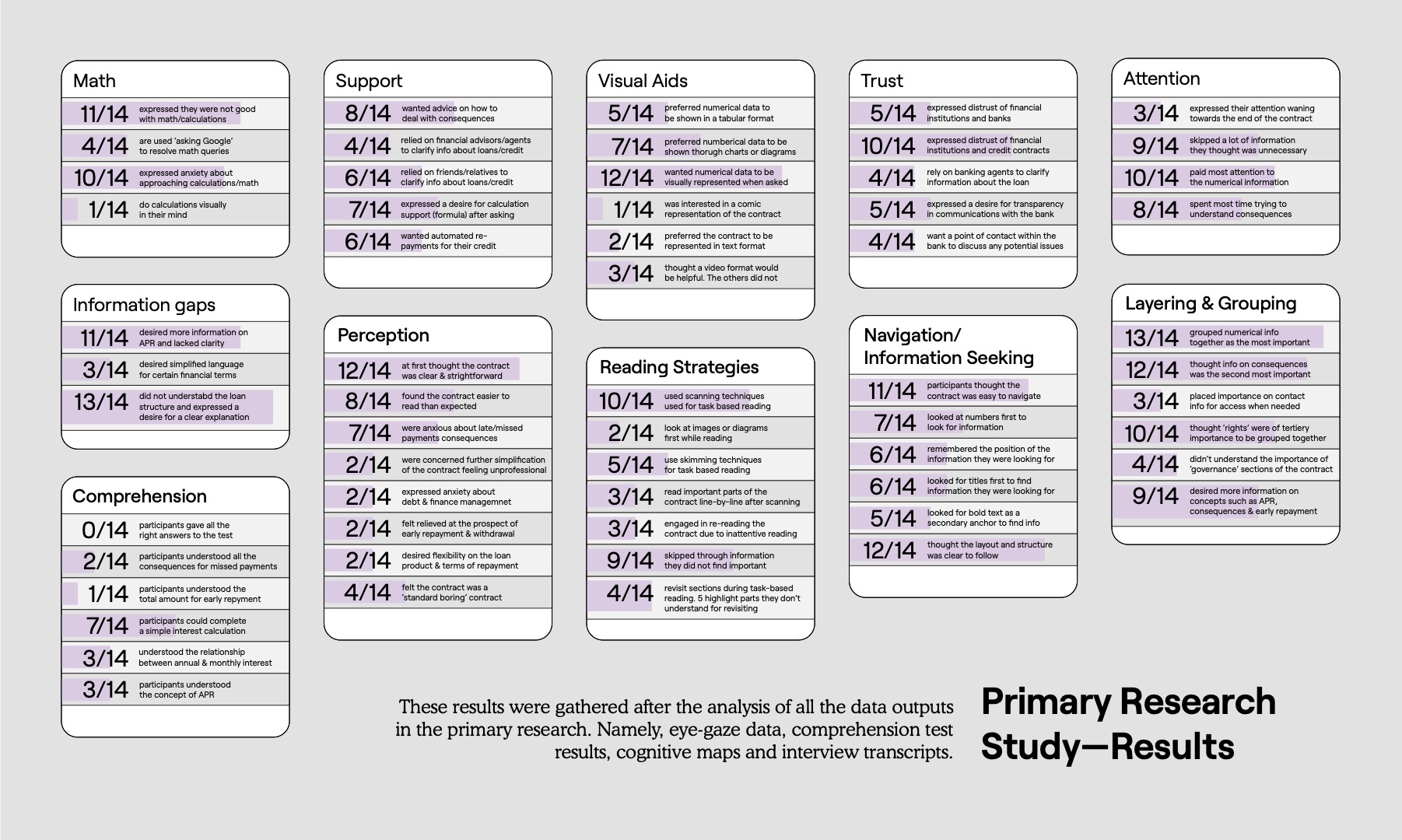

5 Analysis—Summary (Appendix B)

The analysis of the data revealed common themes and challenges for each task:

5.1. Eye-gaze data collection during reading task

Participants were found using various reading patterns, often scanning through the document and fixating on key words/numbers, titles or bold text. Only 4 of 14 participants displayed committed reading patterns (however, in the case of the contract, the committed reading pattern did not correlate with higher comprehension). 10 of 14 users skipped areas of the contract with large blocks of text.

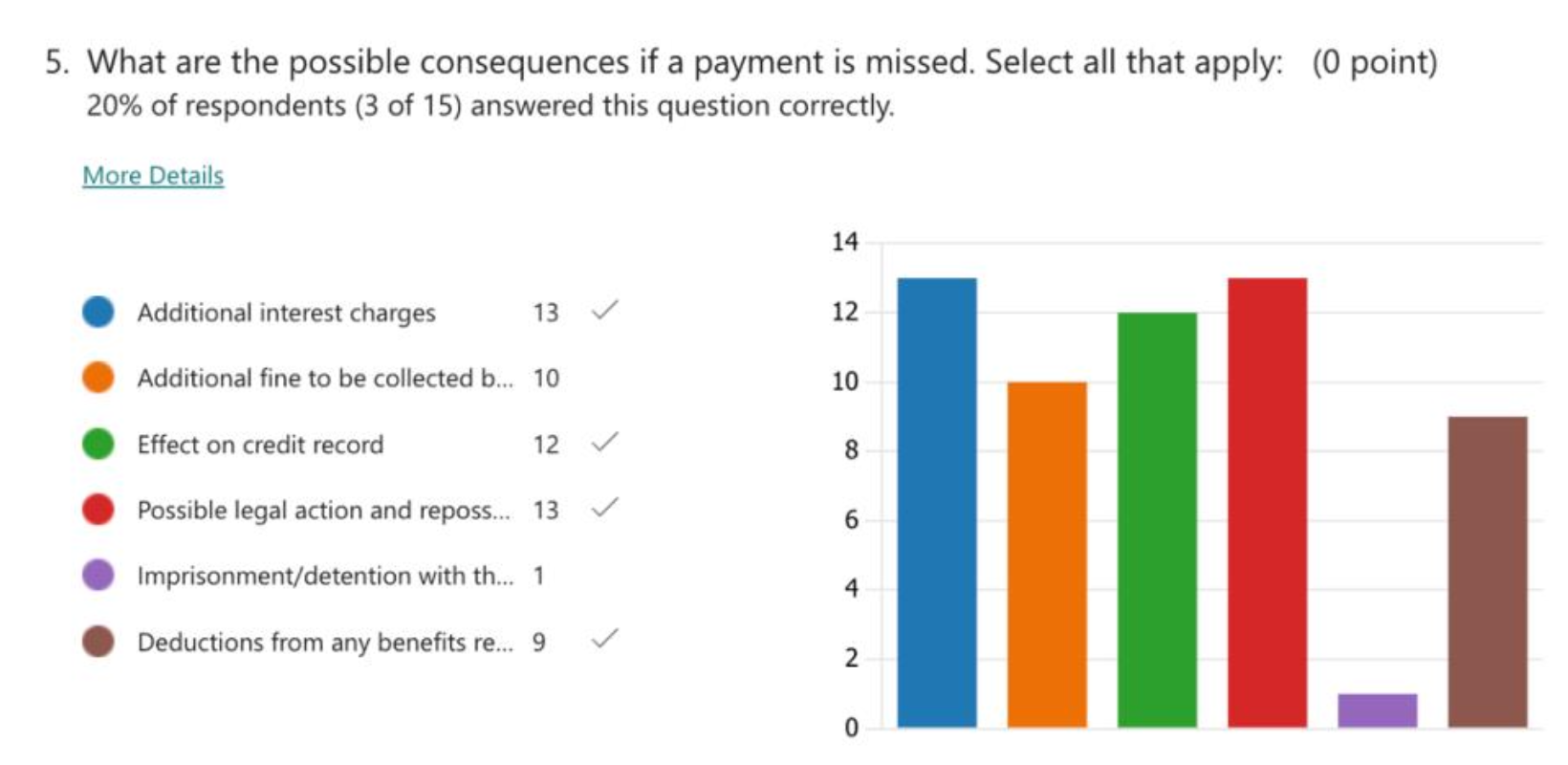

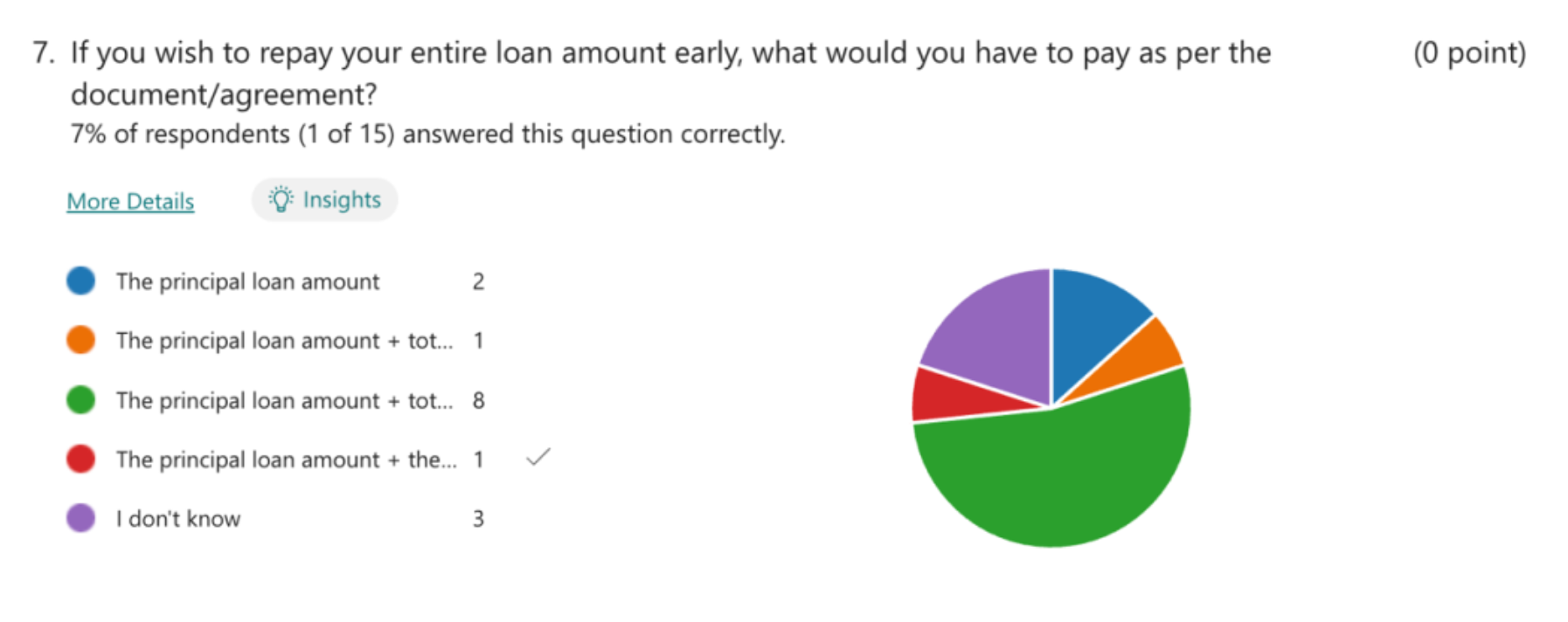

5.2. Comprehension Test

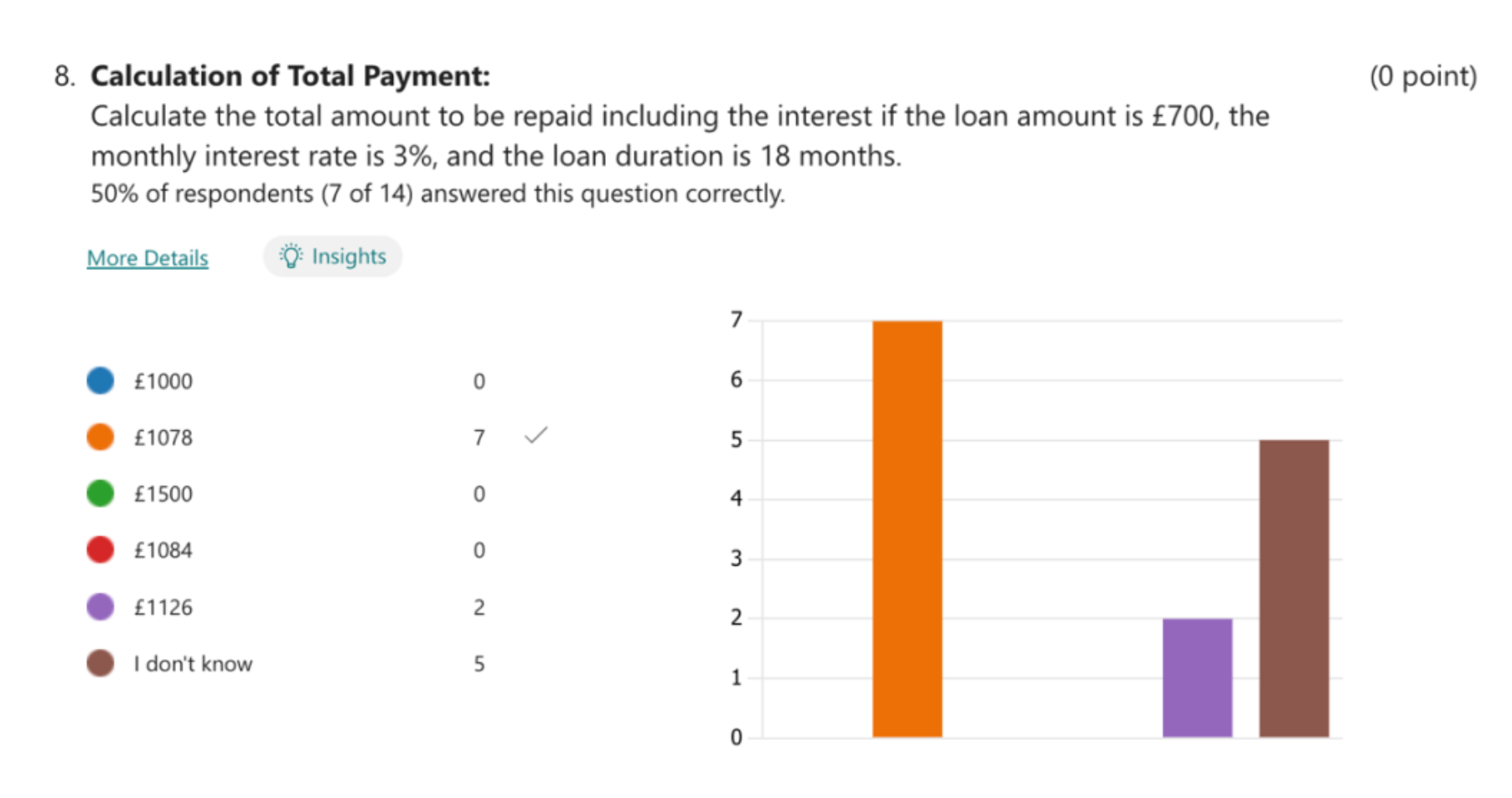

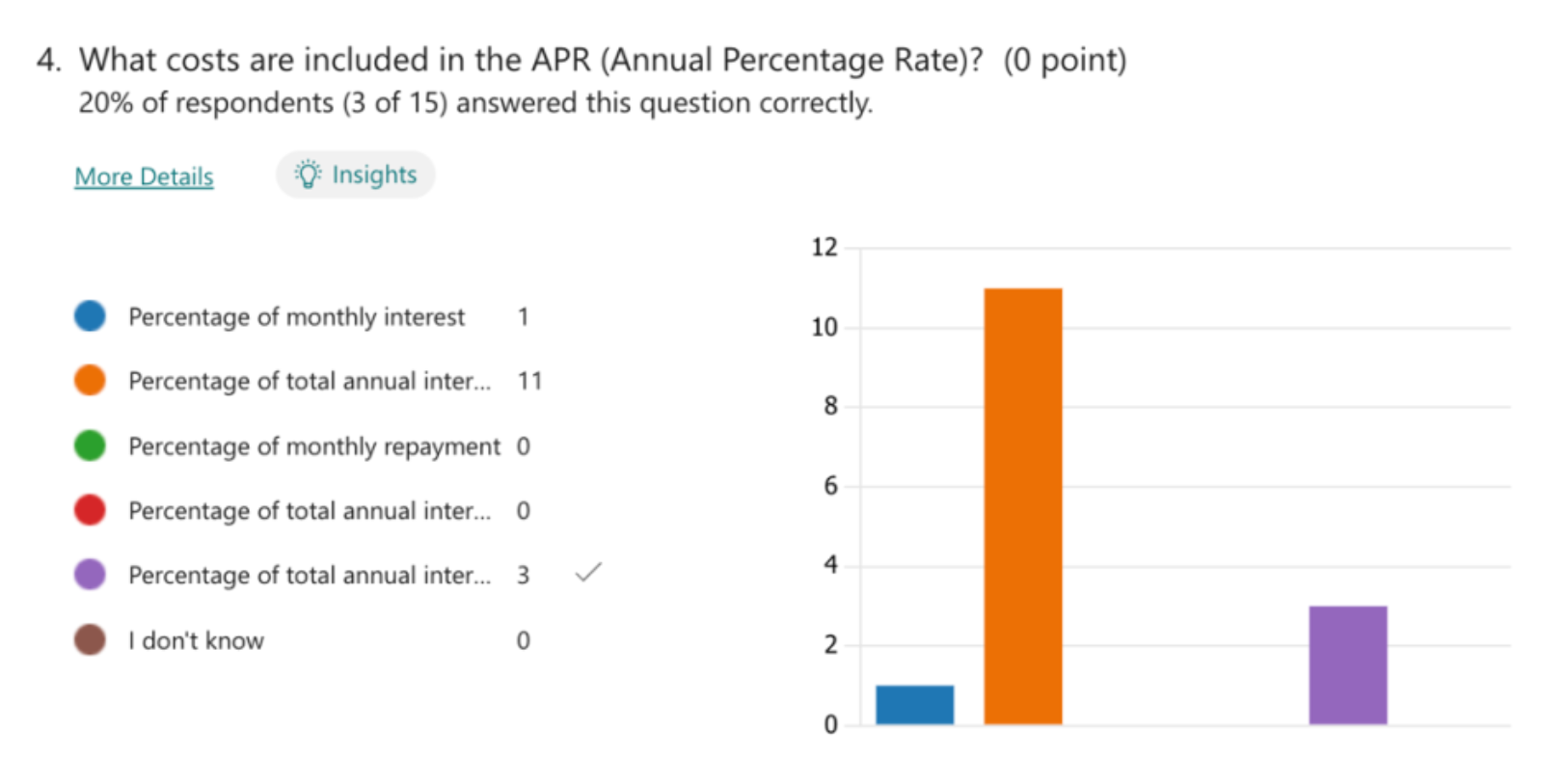

None of the participants were able to get all the answers to the test right. The highest score was 55%. 2 of 14 understood all the consequences of missed payments. 1 of 14 understood the terms of early repayment. 7 of 14 could complete a simple interest calculation and only 3 of 14 understood the breakdown of APR (Annual Percentage Rate).

5.3. Cognitive Mapping Workshop Themes

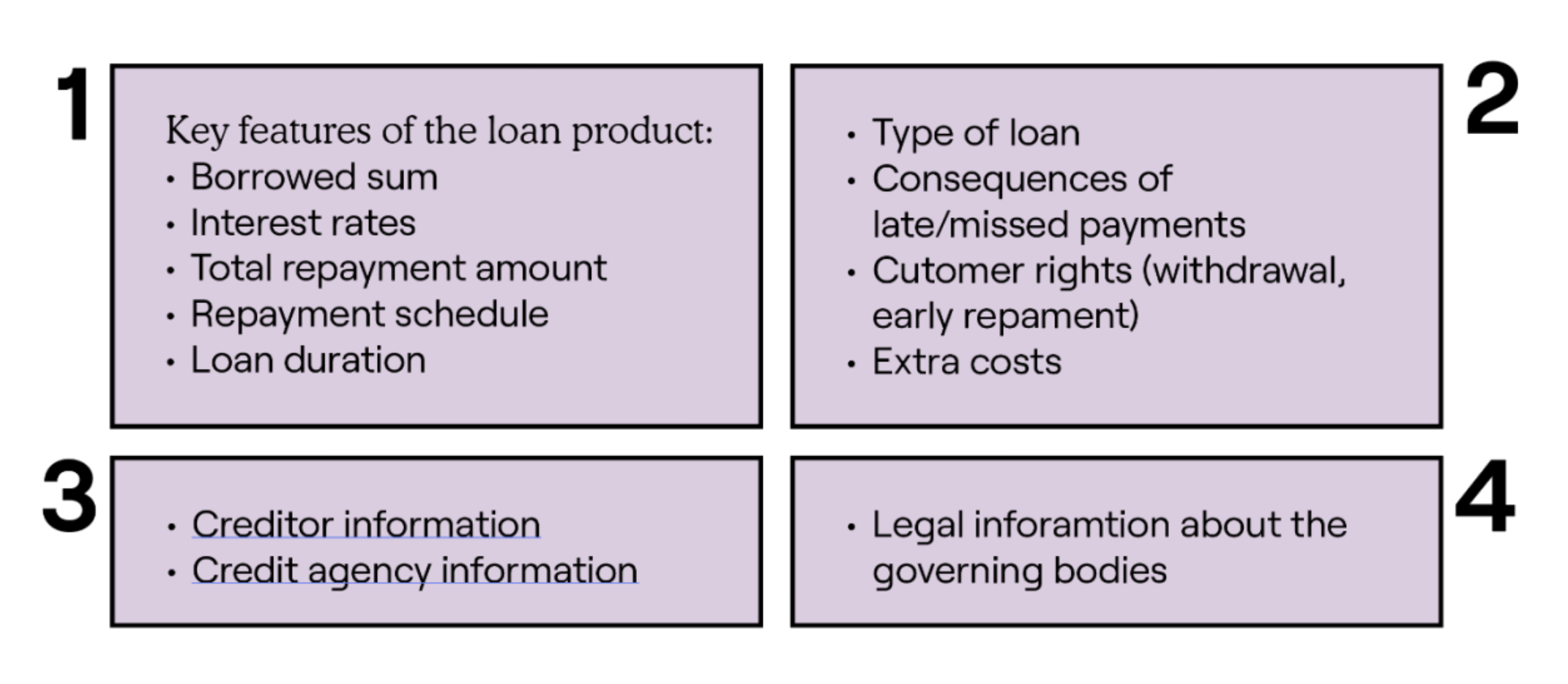

A. Layering and Grouping

Most participants grouped key features/numerical information of the loan product (borrowed sum, repayment sum, interest rate, repayment schedule, and loan duration) as the most important information. At the second tier of importance was the consequences of late/missed payments and tertiary was rights such as early repayment, and withdrawal. Lender details, credit agency and legal was often skipped and users wished to revisit these sections when required.

B. Perception and Emotional Responses

5 of 14 participants expressed fear of debt and 9 of 14 expressed anxiety/apprehension about approaching financial concepts and calculations. 5 of 14 users expressed a distrust of financial institutions/banks.

C. Information Gaps

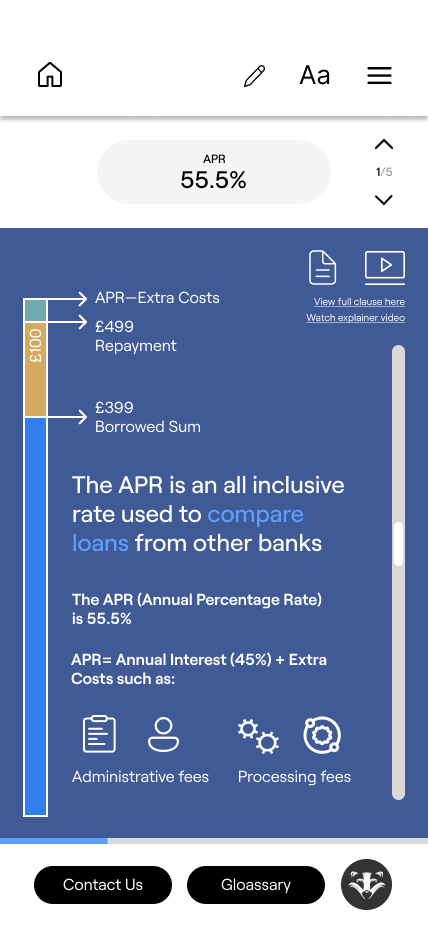

Several information gaps were discovered in the contract that did not allow participants to understand concepts. 11 of 14 participants complained about the lack of clarity on APR and its purpose. 13 of 14 participants, when asked, claimed they understood the loan structure and how interest is calculated—on further probing, it was discovered that they didn’t as the concept is unclear in the contract. The terms of early repayment were not clearly stated in the contract. Participants desired clarity on technical terms such as annual versus monthly interest.

D. Visual aids

10 of 14 participants were interested in the exploration of numerical data and financial concepts explained in tables, charts, or diagrams. 4 of 14 were open to the idea of viewing a video for the contract while 2 of 14 preferred to only read the information.

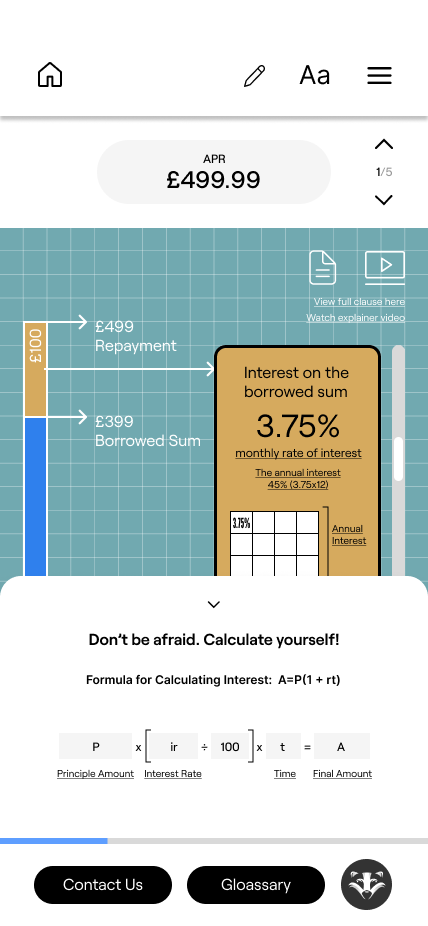

Support Mechanisms: 9 of 14 users, when asked, said a formula for interest would be useful for them to approach calculations due to forgetting the concept in adulthood. 13 of 14 users said they would like to ask an agent/advisor/friend about any doubts they had about the loan and rely of them for clarity. 5 of 14 users spoke about annotating/highlighting strategies to revisit and mark information that requires further clarity.

None of that participants gave all the right answers to the comprehension test

Half of the participants could complete a simple interest calculation

Difficulty in understanding consequences of missed/late payments

Difficulty in understanding the concept of APR

Most attention on numerical information

Desire for visual aids and calculation support

5 Analysis—Summary (Appendix B)

The analysis of the data revealed common themes and challenges for each task:

5.1. Eye-gaze data collection during reading task

Participants were found using various reading patterns, often scanning through the document and fixating on key words/numbers, titles or bold text. Only 4 of 14 participants displayed committed reading patterns (however, in the case of the contract, the committed reading pattern did not correlate with higher comprehension). 10 of 14 users skipped areas of the contract with large blocks of text.

5.2. Comprehension Test

None of the participants were able to get all the answers to the test right. The highest score was 55%. 2 of 14 understood all the consequences of missed payments. 1 of 14 understood the terms of early repayment. 7 of 14 could complete a simple interest calculation and only 3 of 14 understood the breakdown of APR (Annual Percentage Rate).

5.3. Cognitive Mapping Workshop Themes

A. Layering and Grouping

Most participants grouped key features/numerical information of the loan product (borrowed sum, repayment sum, interest rate, repayment schedule, and loan duration) as the most important information. At the second tier of importance was the consequences of late/missed payments and tertiary was rights such as early repayment, and withdrawal. Lender details, credit agency and legal was often skipped and users wished to revisit these sections when required.

B. Perception and Emotional Responses

5 of 14 participants expressed fear of debt and 9 of 14 expressed anxiety/apprehension about approaching financial concepts and calculations. 5 of 14 users expressed a distrust of financial institutions/banks.

C. Information Gaps

Several information gaps were discovered in the contract that did not allow participants to understand concepts. 11 of 14 participants complained about the lack of clarity on APR and its purpose. 13 of 14 participants, when asked, claimed they understood the loan structure and how interest is calculated—on further probing, it was discovered that they didn’t as the concept is unclear in the contract. The terms of early repayment were not clearly stated in the contract. Participants desired clarity on technical terms such as annual versus monthly interest.

D. Visual aids

10 of 14 participants were interested in the exploration of numerical data and financial concepts explained in tables, charts, or diagrams. 4 of 14 were open to the idea of viewing a video for the contract while 2 of 14 preferred to only read the information.

Support Mechanisms: 9 of 14 users, when asked, said a formula for interest would be useful for them to approach calculations due to forgetting the concept in adulthood. 13 of 14 users said they would like to ask an agent/advisor/friend about any doubts they had about the loan and rely of them for clarity. 5 of 14 users spoke about annotating/highlighting strategies to revisit and mark information that requires further clarity.

Brief

Design a mobile interface that clearly presents key loan features and consequences. Reorganize content by importance and logic, addressing gaps through layered information. Visually map numerical data to improve understanding and reduce anxiety. Explore support tools to ease math-related stress and boost engagement.

6.1. Problem statement

Based on the findings from the study, the following problem statement was arrived at, placing a priority on common high impact problems:

Consumers of financial contracts (especially novice consumers) often find the contracts to be cumbersome and confusing to read. Despite the potential short length of a contract and perceived comprehension of the same, users do not grasp concepts within the contract, financial or otherwise. There exist information gaps in credit contracts that do not allow users to comprehend all the necessary information. These contracts tend to have large chunks of text easily ignored by users, where they may miss important information. Further, users are apprehensive of financial institutions, debt, and doing necessary basic calculations needed to understand credit products by themselves.

6.2. Brief

Explore designs for a mobile application interface with a focus on key features of the loan product and consequences. Re-group information by importance and logic, while addressing information gaps through layers. Visually map the journey of the numerical information in the loan to increase comprehension of and engagement with the information, whilst reducing anxiety. Explore support mechanisms that can reduce anxiety about math and consequences/debt and increase ease of comprehension and engagement.

Opportunities

Visualise information engagingly

Provide support mechanisms for calculations

Create interactive experiences for financial information

Layer and link concepts through layers to reduce cognitive load

Provide advice for consequences

Consider different user journeys & highlight important information

6.1. Problem statement

Based on the findings from the study, the following problem statement was arrived at, placing a priority on common high impact problems:

Consumers of financial contracts (especially novice consumers) often find the contracts to be cumbersome and confusing to read. Despite the potential short length of a contract and perceived comprehension of the same, users do not grasp concepts within the contract, financial or otherwise. There exist information gaps in credit contracts that do not allow users to comprehend all the necessary information. These contracts tend to have large chunks of text easily ignored by users, where they may miss important information. Further, users are apprehensive of financial institutions, debt, and doing necessary basic calculations needed to understand credit products by themselves.

6.2. Brief

Explore designs for a mobile application interface with a focus on key features of the loan product and consequences. Re-group information by importance and logic, while addressing information gaps through layers. Visually map the journey of the numerical information in the loan to increase comprehension of and engagement with the information, whilst reducing anxiety. Explore support mechanisms that can reduce anxiety about math and consequences/debt and increase ease of comprehension and engagement.

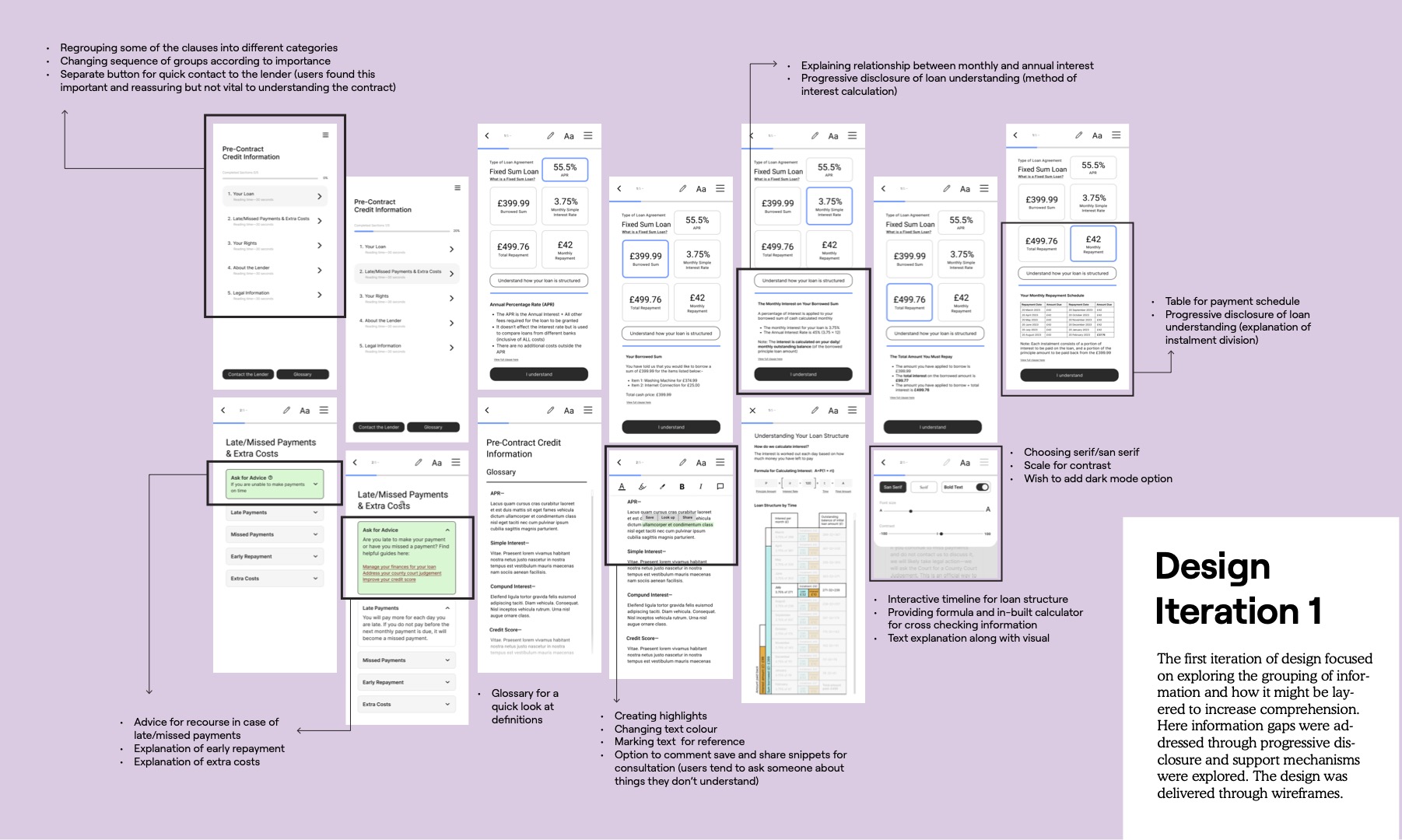

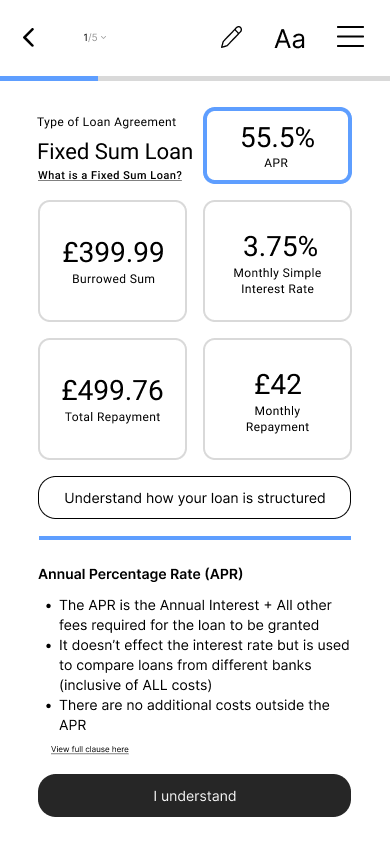

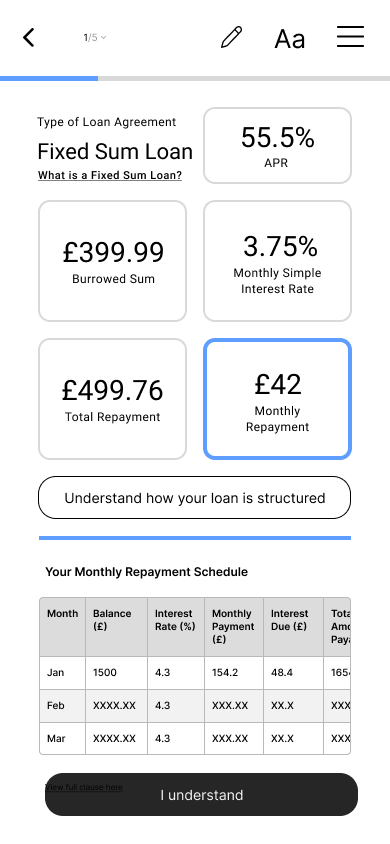

Design Iteration I

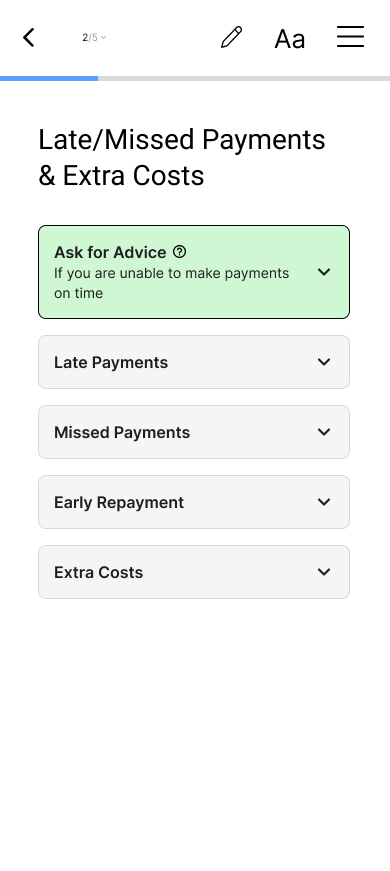

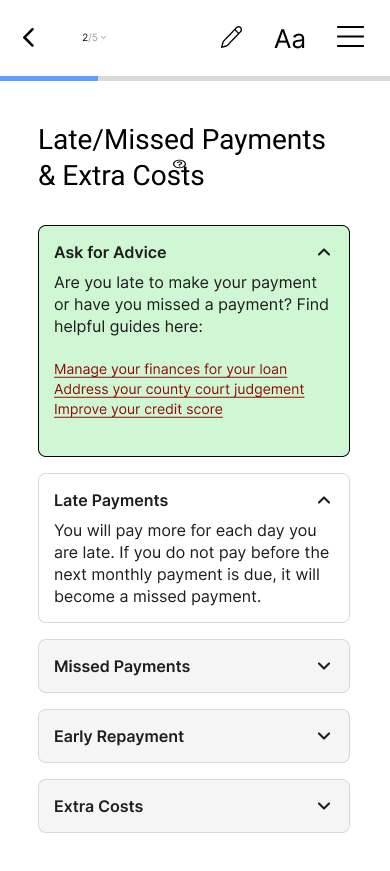

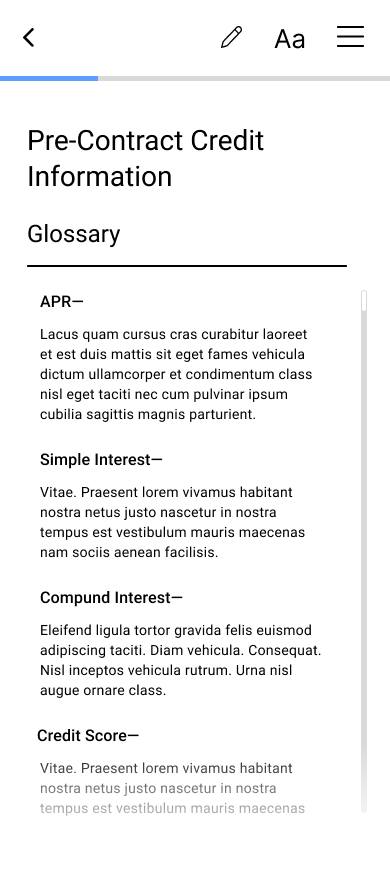

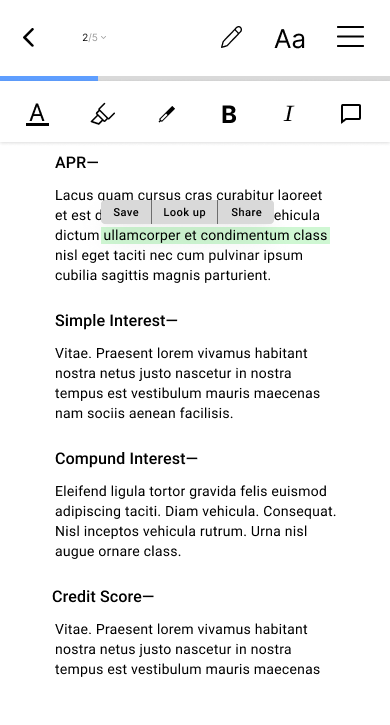

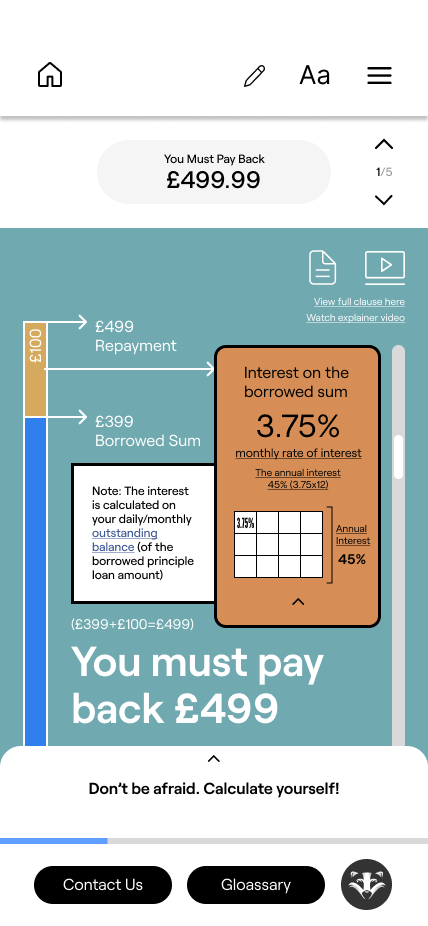

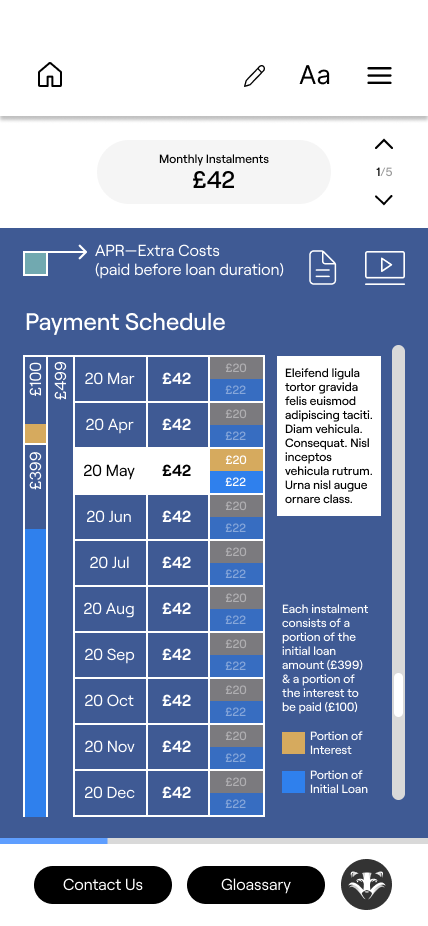

Contract information was restructured for clarity and relevance, supported by visual tools like loan timelines, repayment tables, and an in-app calculator. Progressive disclosure, glossaries, and layered explanations helped simplify complex content. Readability was enhanced through customisable text and highlight/save functions. The design also introduced support flows for missed payments, early repayment, and additional costs, while offering reassurance through direct lender contact and contextual guidance.

7. Design & Testing

The design for a mobile application was explored in iterations focusing on explorations of visual mapping of financial data, layering information and possible support functions.

For testing different iterations of the design, ‘Heuristic Evaluation’ (Nielsen, 2024) and ‘Usability Tests’ (Moran, 2023) were employed using an exploratory framework.

7.1. Ideation Sketches

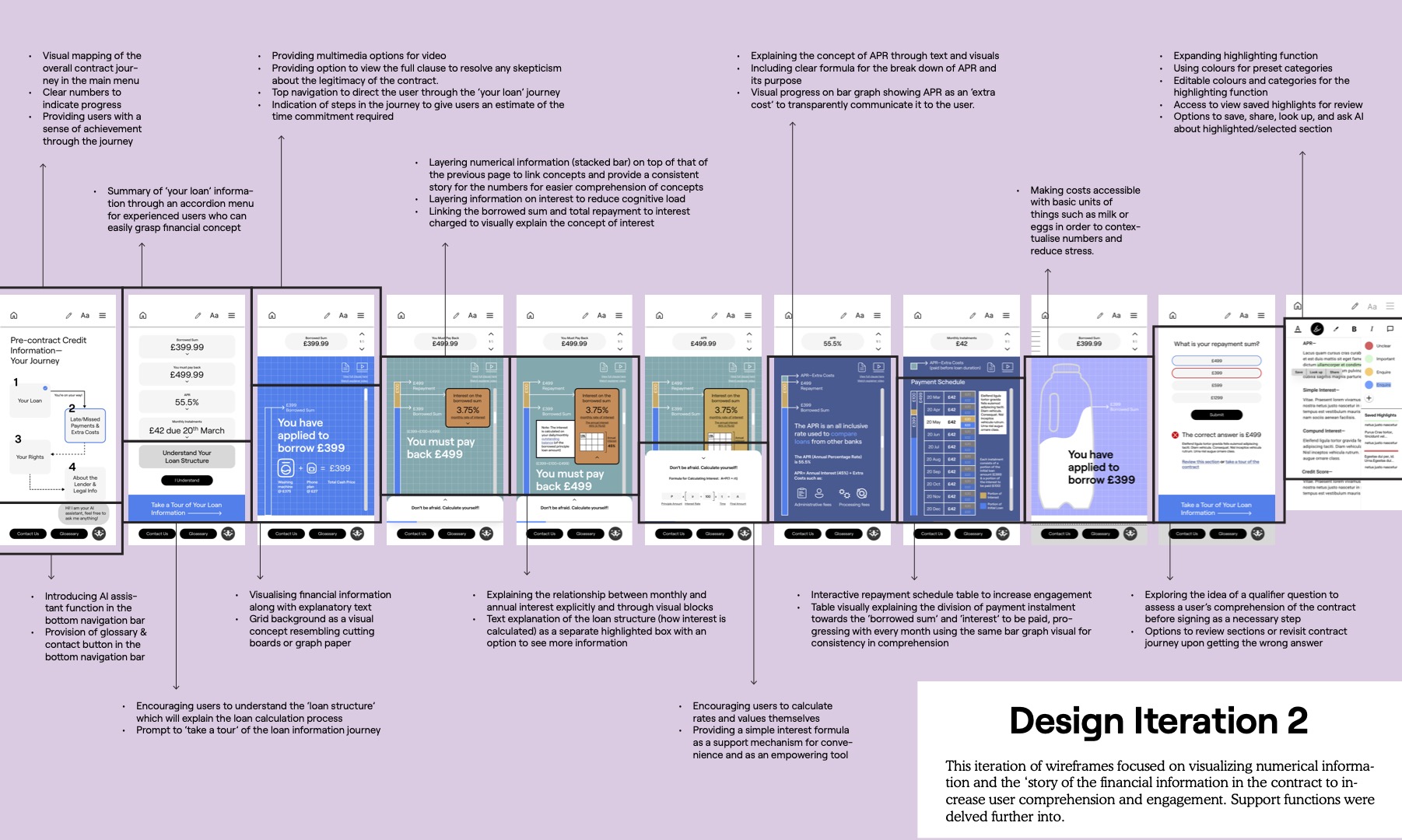

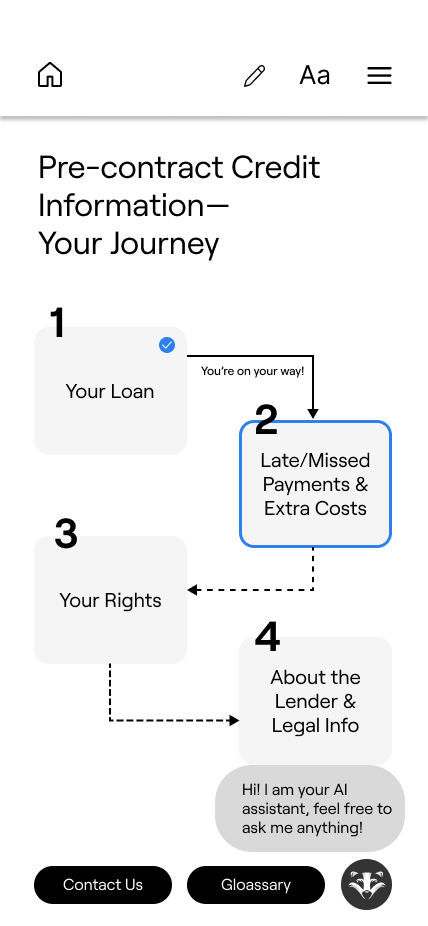

7.2. Design Iteration 1

The first iteration of design focused on exploring the grouping of information and how it might be layered to increase comprehension. Here, information gaps were addressed through progressive disclosure and support mechanisms were explored. The design was delivered through wireframes.

A. Feedback from External Supervisors (Amplifi, UK)

Key Takeaways

- Focus on ‘numerical loan information’

- Make financial info more visual & layered

- Consider AI assistant functionality

- Think about expanding highlighting function

- Consider visual mapping for navigation Simplify ‘loan structure’ table

- Add multi-media functions

Design Iteration II

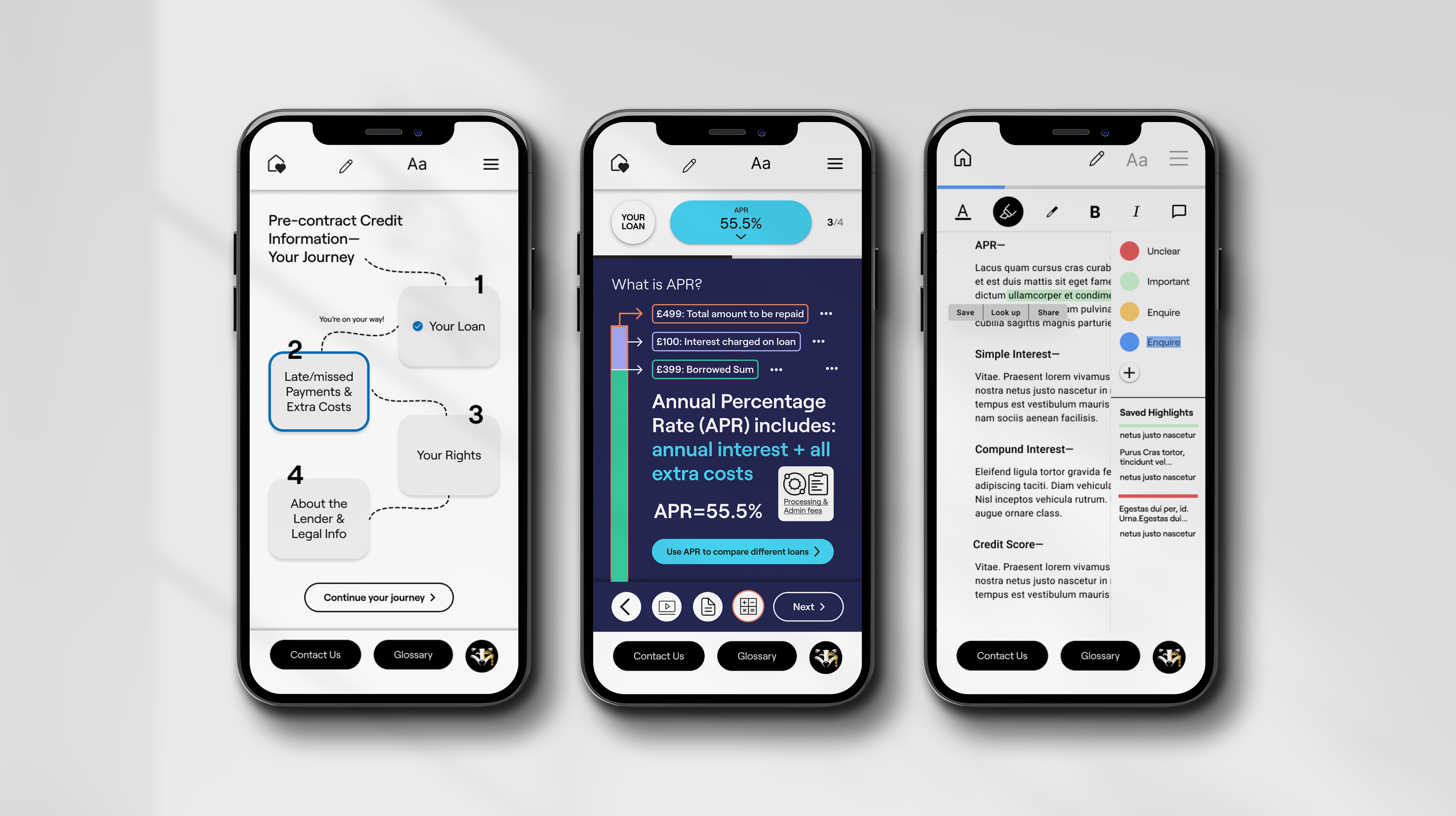

The contract journey was mapped with clear progress indicators and visual layers, such as bar graphs and interest breakdowns, to reduce cognitive load. Financial figures were contextualised using relatable everyday units. Interactive tools—including calculators, repayment tables, and qualifier questions—were introduced to support informed decision-making. Key features like an AI assistant, glossary, and clause access were integrated, along with highlight, save, and share options to give users greater control and recall.

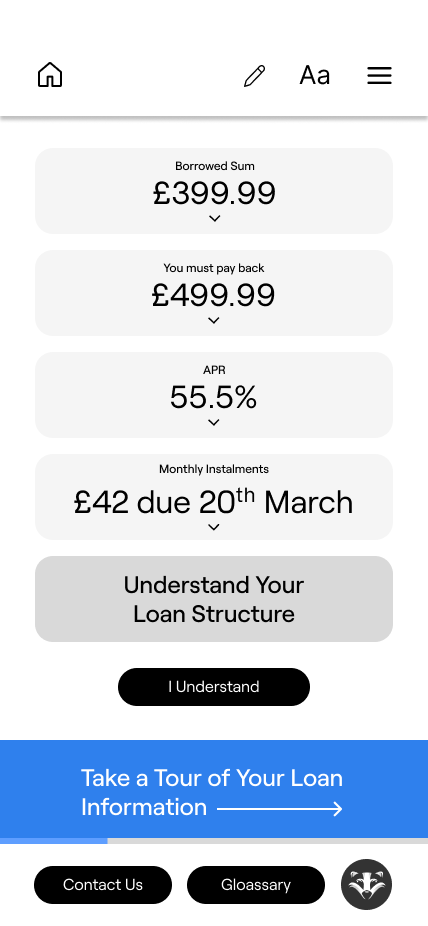

7.3. Design Iteration 2

This iteration of wireframes focused on visualising numerical information and the ‘story of the financial information’ in the contract to increase user comprehension and engagement. Support functions were further delved into.

A. Testing Round 2—Heuristic Evaluation (Appendix D)

Key takeaways

- Focus on numbers narrative for comprehension—simplify repayment table

- Make visuals clear (remove grid background)

- Expand calculator support for prototype

- Simplify ‘Repayment Schedule’ table

- Standardise colours and their function

- Introduce AI assistant clearly

- Make navigation within sections more prominent

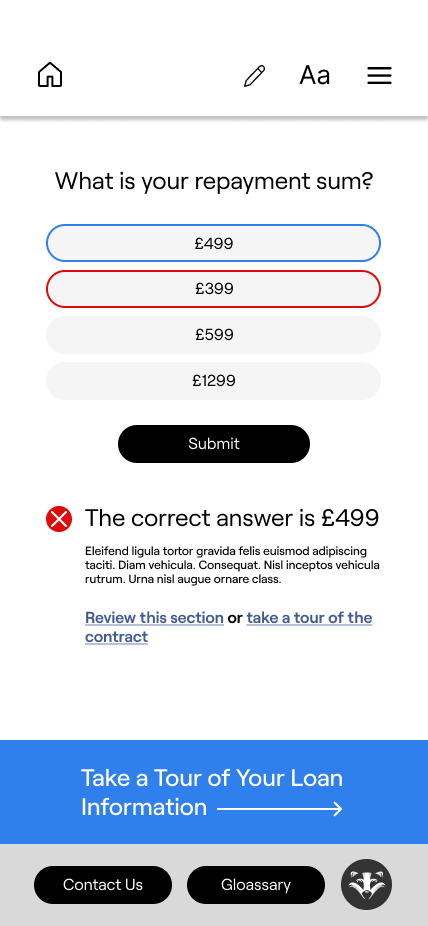

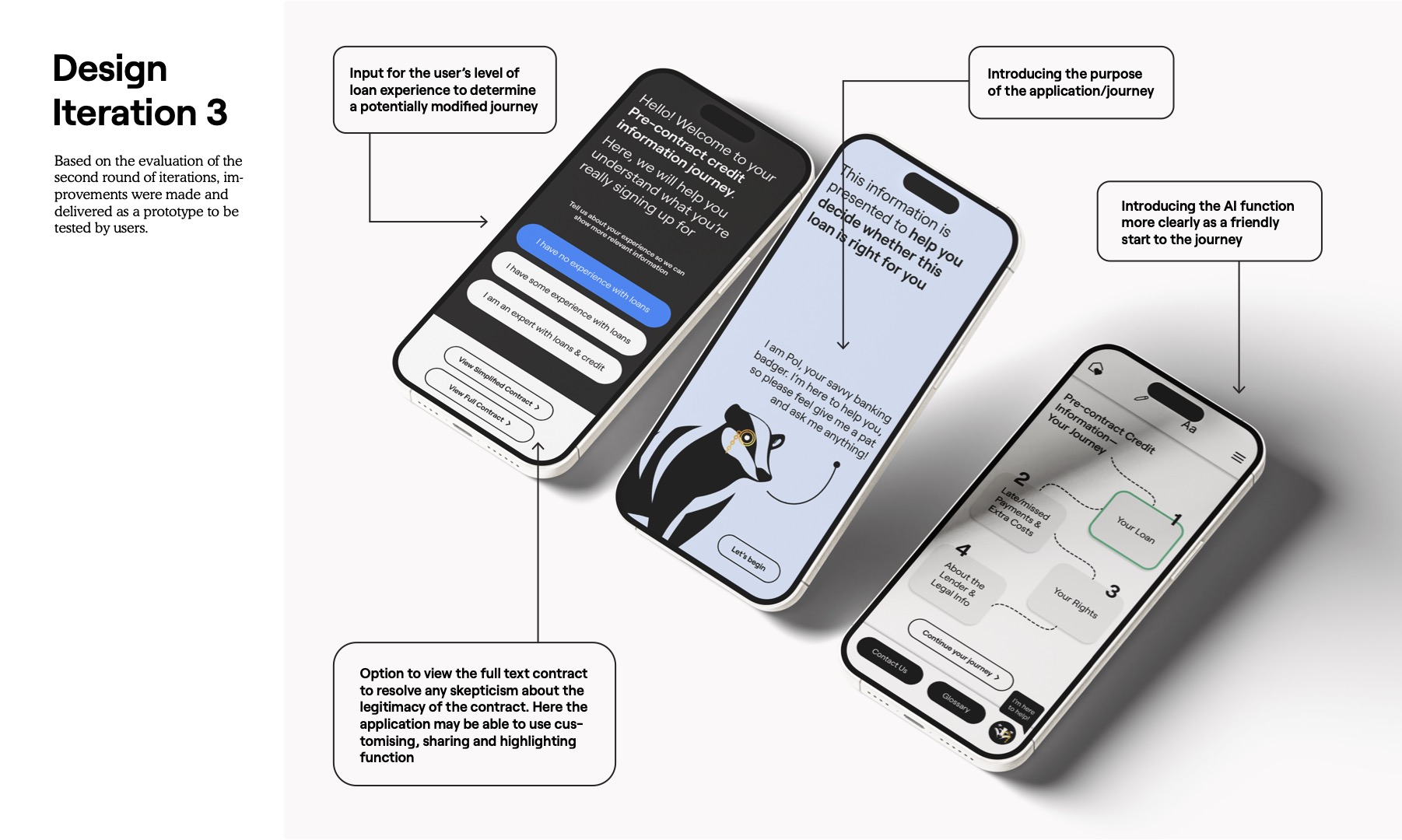

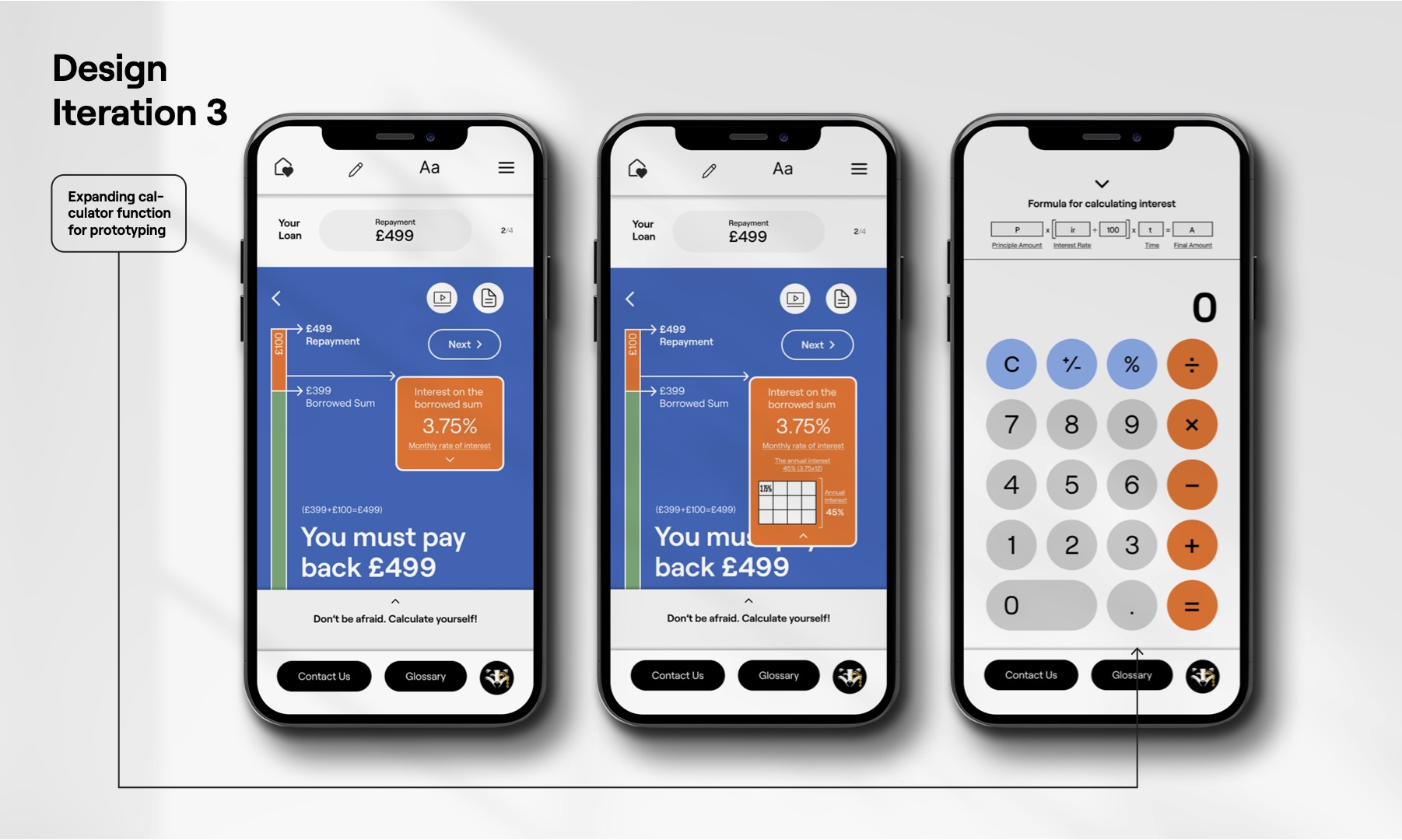

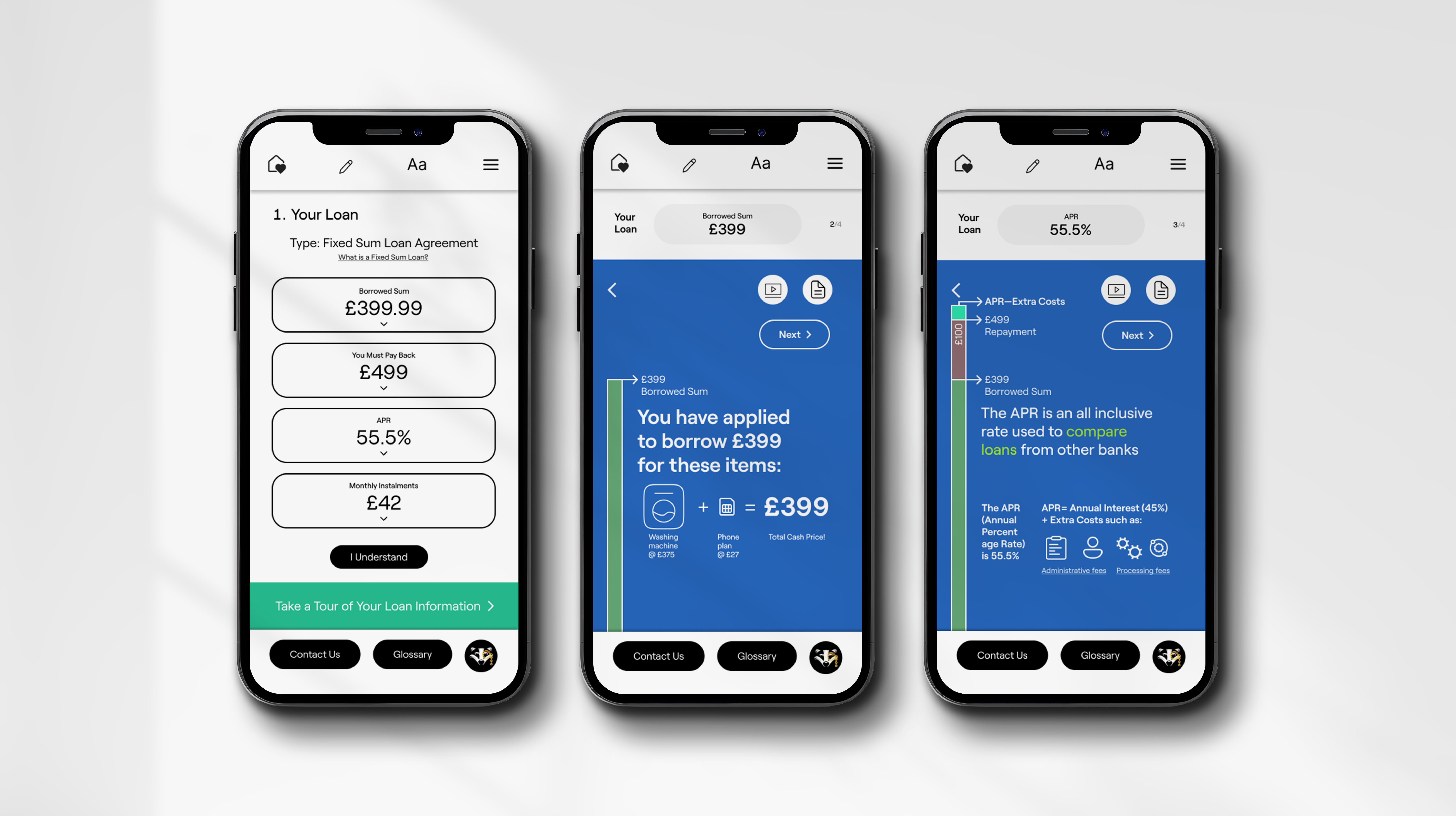

Design Iteration III

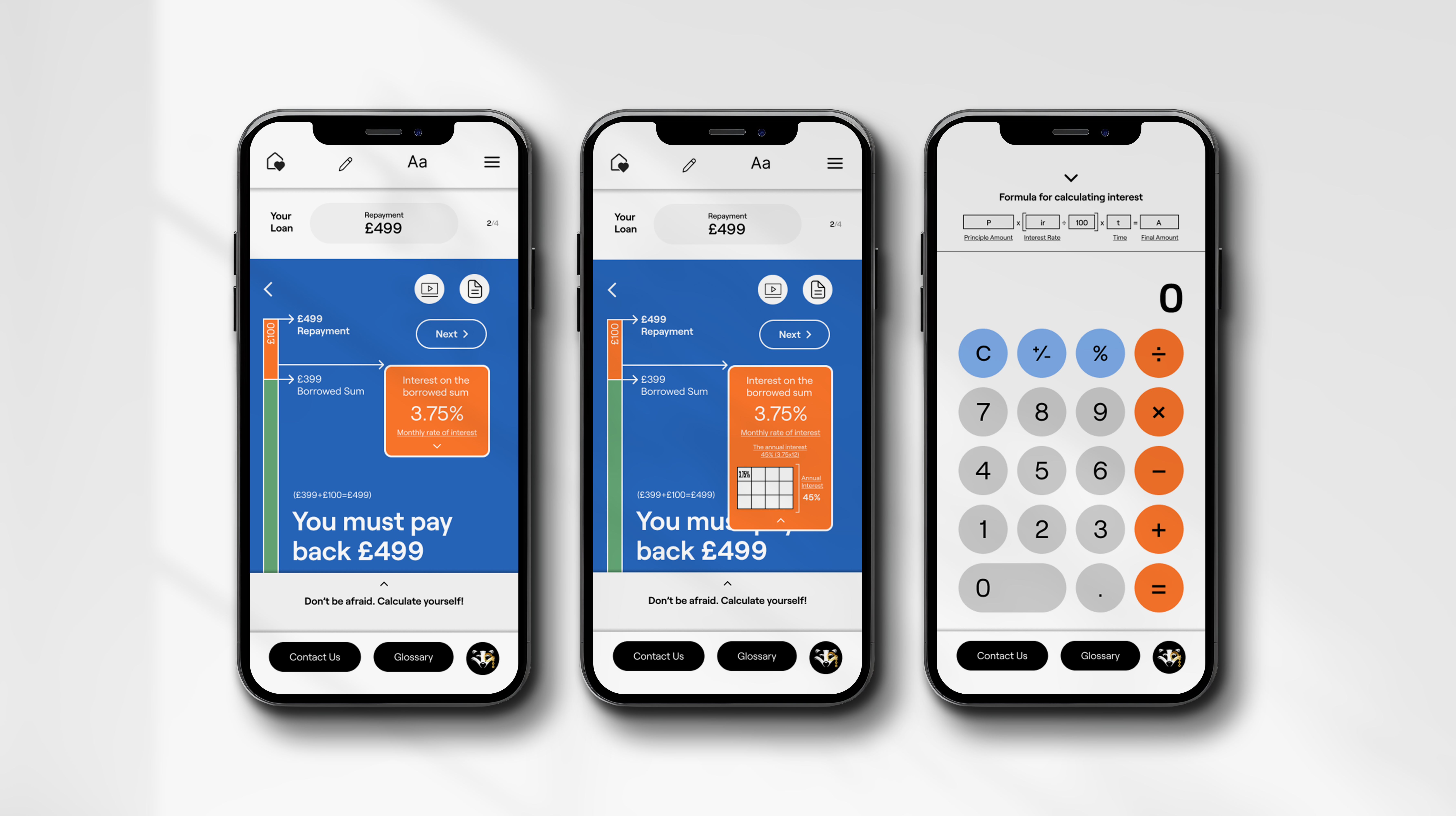

The interface was tailored to users’ loan experience, with a clear intro, guided AI support, and intuitive navigation. Visual clarity was enhanced through consistent colours, simplified layouts, an expanded calculator, and an interactive repayment table for easier understanding.

7.4. Iteration 3

Based on the evaluation of the second iteration, improvements were made and delivered as a prototype to be tested by users.

Happy path for prototype: home > your loan > borrowed sum > repayment sum > APR > payment schedule

Prototype Link: Iteration 3—Prototype

Usability Test—Action Items

Information Clarity: Reorder content for logical flow

User Segmentation: Tailor complexity of financial info based on user experience level

Content Gaps: Add missing details like loan duration, APR fees, and tooltips for definitions

Navigation Consistency: Standardise bottom nav and interactive elements (e.g. accordions)

Visual Refinement: Improve colour contrast, larger text, and clearer call-to-action buttons

8. Evaluation

8.1. Evaluation Plan (see Appendix D for details)

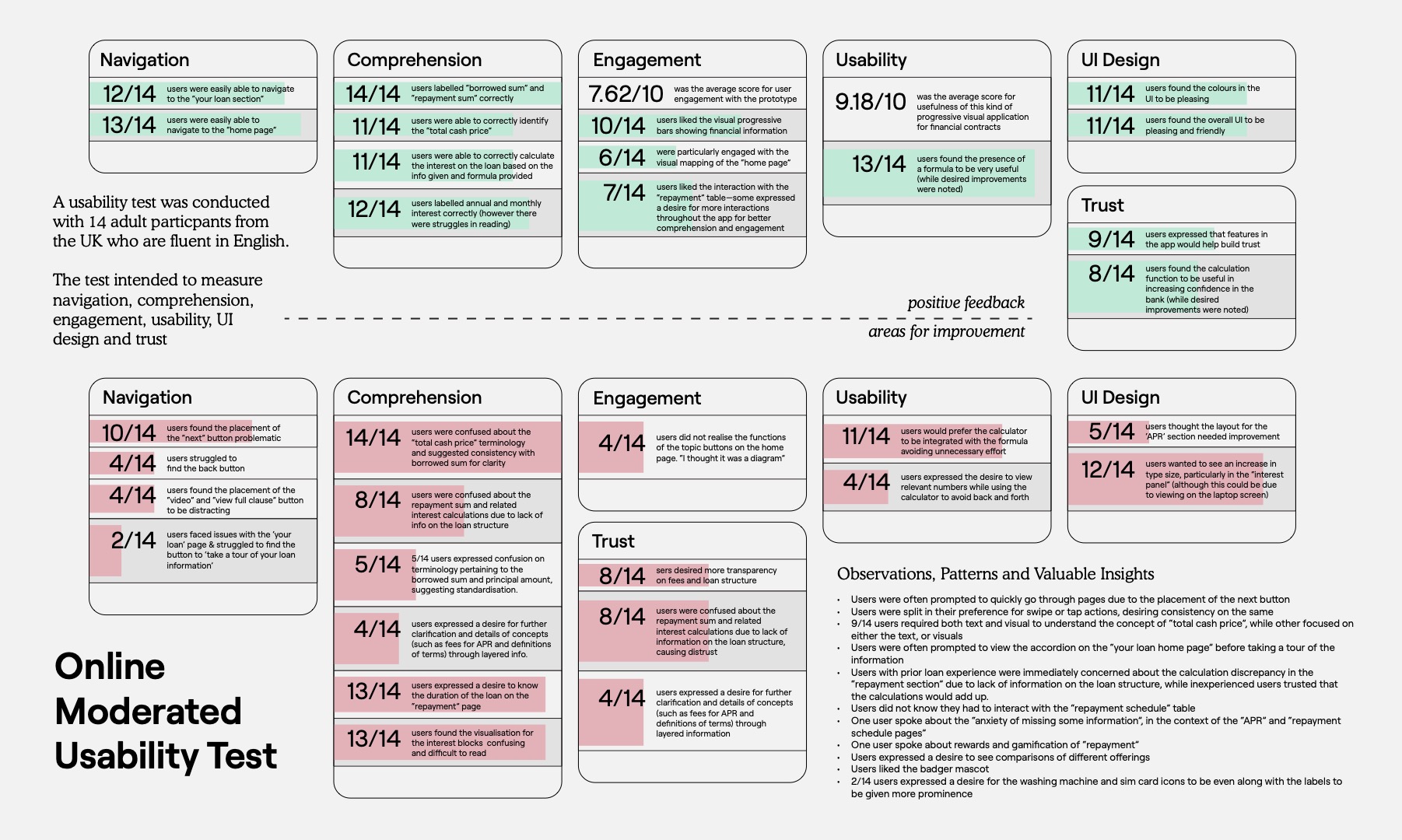

An online moderated usability test of the prototype was then conducted with 14 participants to test the following:

- Navigation

- Usability

- Comprehension

- Engagement

8.2. Results (see Appendix D for details)

Key takeaways

- Re-arranging and grouping information: sequence—repayment schedule at repayment section.

- Consider user group for disclosure of complex financial concepts such as the entire loan structure. This information can confuse novice users while the lack of it, confuses users with prior loan or financial experience.

- Information Gaps: Duration of loan, APR fees, tooltips with definitions.

- Navigation fixes: consistent bottom navigation for your loan, keep consistent navigation elements such as on-click accordions.

- Design changes: improve colours for engagement and contrast, increase text sizes, making certain buttons more prominent.

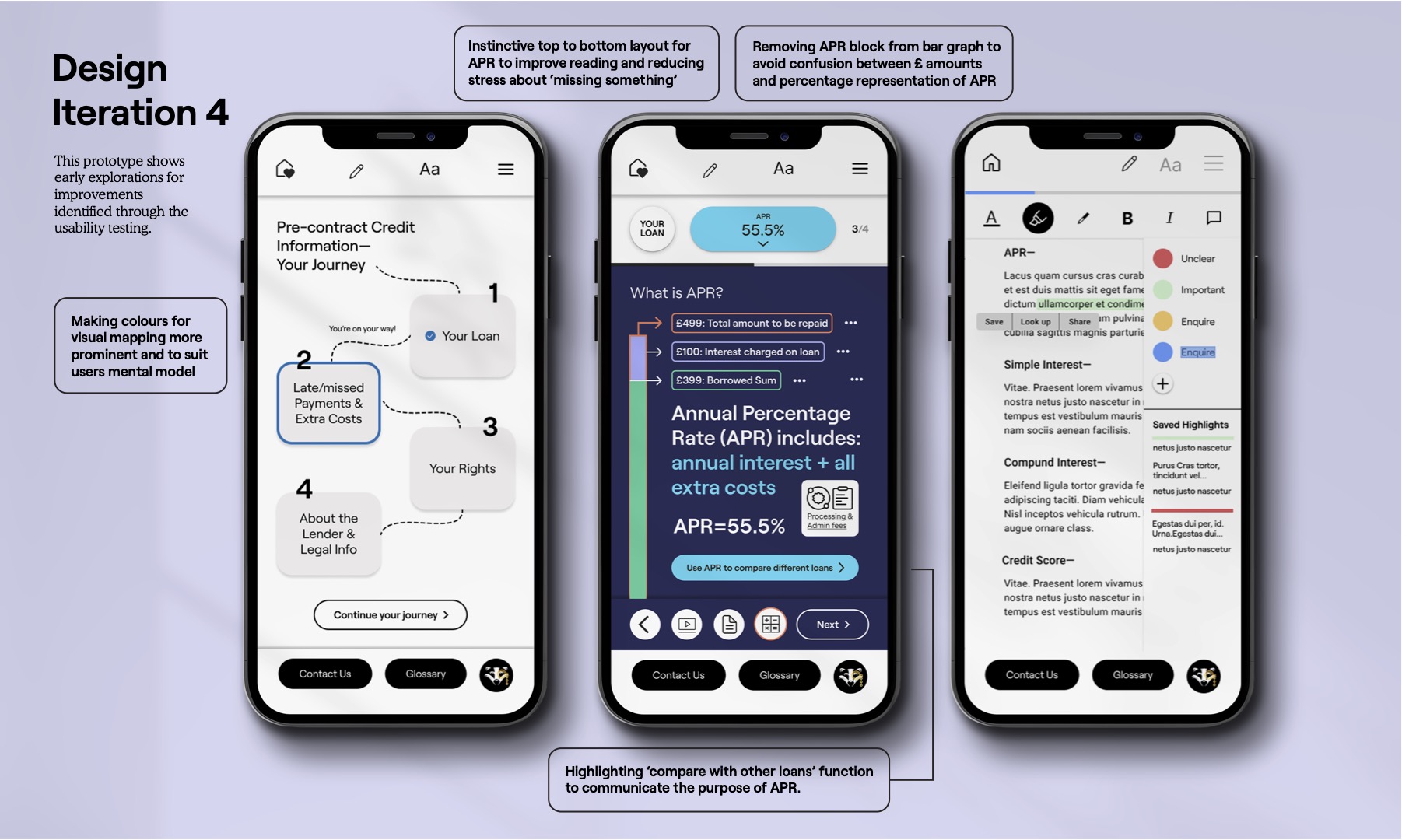

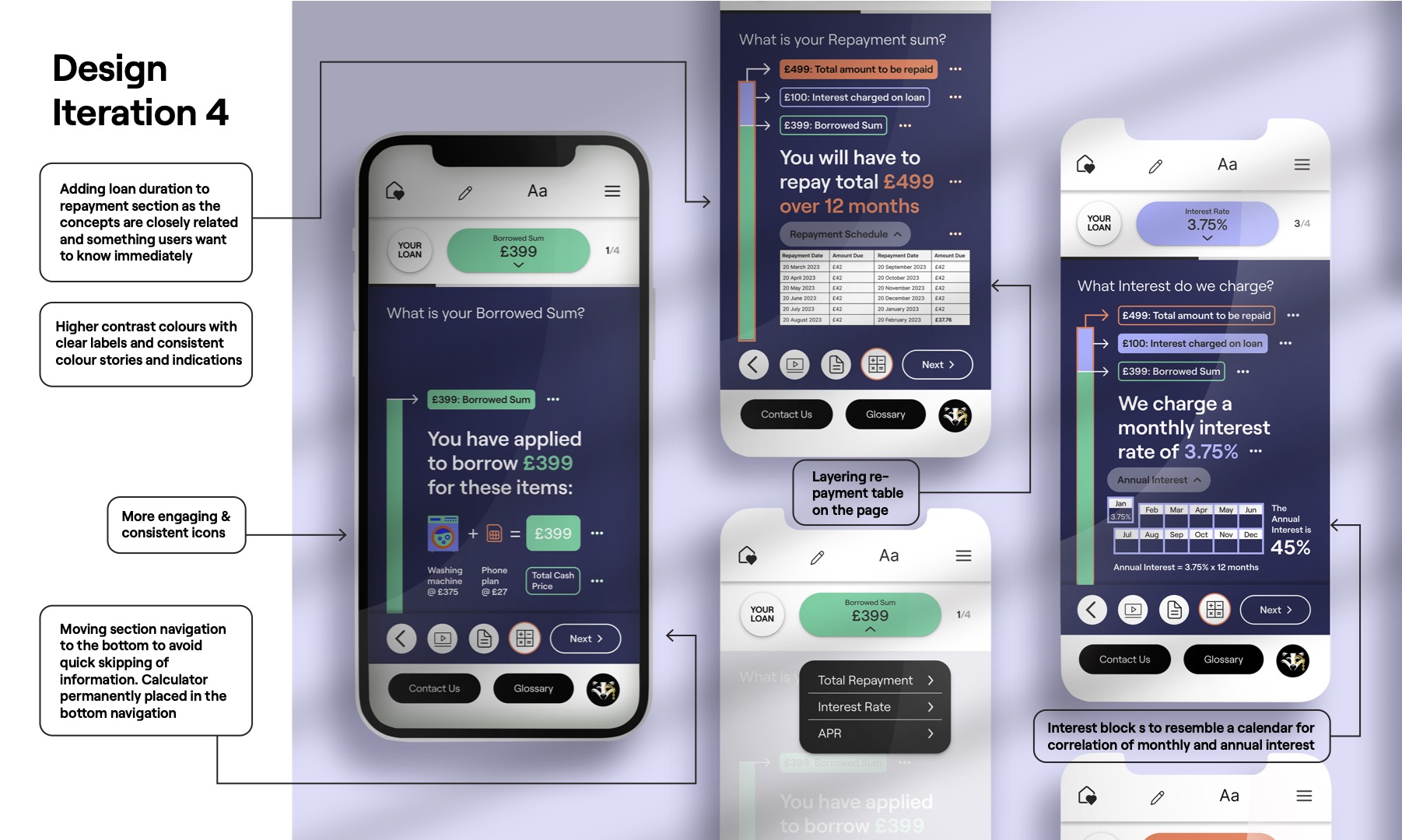

8.3. Redesign Exploration

This prototype shows early explorations for improvements identified through the usability testing.

Prototype link: Iteration 4—Prototype

Final Iterations 👀

Refinements focused on improving clarity, navigation, and financial comprehension:

Improved colour contrast, icon consistency, and visual hierarchy

Streamlined APR layout and removed overlapping visuals

Linked loan duration with repayment info for better context

Added titles, tooltips, and calendar-style interest display

Enhanced navigation with clearer buttons and persistent tools

Recommendations

Simplify Content: Reduce text density and use progressive disclosure

Enhance Calculator: Streamline inputs and integrate calculations into formulas

Clarify Terminology: Standardise labels and add tooltips for financial terms

Improve Visual Design: Adjust fonts, boost contrast, and reduce clutter

Refine Navigation: Standardise button placement and enhance element clarity

Add Features: Include fee breakdowns, glossary, and comparison tools

9. Conclusion

9.1. Design Recommendations

- Add tooltips for technical definitions as a layer of information

- Disclose ‘Loan Structure’ Calculations and methods in a layer during the journey of financial information. Give a text indication about how the interest is calculated on the daily outstanding balance on the interest/repayment page and add a layer visually explaining the entire structure. Experienced users will immediately get the clarity they need as they are calculating interest and novice users will be able to digest this information if they choose to, without increasing cognitive load.

- Standardise terminology throughout the contract to avoid confusion—two terms that essentially mean the same thing should not be used.

- Integrate calculator with formula with multiple options to fill values instead of having only custom inputs. Provide clarity on the units within the formula

- Explore gamification of the repayment table to provide a sense of achievement

9.2. Research Questions—Answers & Discussion

While layered visual financial contracts can improve comprehension and engagement, it is vital to understand the content and how users perceive financial data and how to tell ‘the story of it’. Simplified contracts can boost confidence in approaching such content. However, the question of tackling math/calculations must be explored further to understand user’s preferred methods of calculation and overall experiences with math. Provision of a calculation formula, while proving convenient, may not be sufficient in enhancing confidence. The simplification, visual layering and support mechanisms within such contracts can encourage transparency and foster trust. It is also dependent on the commitment of financial institutions to reveal key information (such as that of loan structure and minimum repayments). Attitudes towards reliability of information (especially once it is simplified) are often shaped by brand and reputation. Further, in reducing cognitive load through simplified visual layering, users may also feel like ‘they’ve missed something’ and can be explored further as a concept.

The impact of such work may be significant in the field of Legal Design. Using more participatory methods and working with policy makers to set benchmarks and policy for financial contracts in the UK, as undertaken by Amplifi, UK, is an important step in increasing the financial capabilities and health of the population. As seen, such work is already being undertaken and much is yet to be explored—especially in the realm of finance where numerical data and concepts must be effectively understood. Such learnings may also be applied to financial data for more complex instruments such as long-term debt management, shares, securities, funds and other investments.

9.3. Limitations & Future Work

This research study was conducted with participants with high levels of literacy. Users with low levels of literacy must be considered while thinking about larger systems for increasing the financial ability of a population.

As the designs for this project aimed to explore specific concepts freely, they did not provide insights that more detailed prototypes would about navigation, design and interaction.

Since the designs were exploratory, accessibility was not thoroughly considered in the prototypes. Basic principles such as contrast and sizes were considered. However, to make this design viable and equitable, accessibility thinking must be incorporated into the design and research process.

Users with varying experiences must be considered for the successful communication of financial legal content. While hiding something may help novice users reduce cognitive load, it may confuse more experienced users.

There were many ideas for functions explored for this design research study, however due to lack of time, they were not all able to be fleshed out and tested. Functions such as annotations, revisiting, qualifying questions to ensure comprehension before signing, sharing information, customizing the interface, and the AI assistant may be explored further to inform the overall contract journey.

The concept of gamification and increased interaction can be incorporated into various parts of the contract journey, such as calculation and repayment to improve user engagement and comprehension.